As the luck of the Irish would have it, we’re kicking off this week’s produce industry newsletter with updates that might make you feel like you’ve found a pot of gold.

Snow in Colorado might have halted transportation in the Four Corners region, but fear not… Shippers should iron out regional supply chains over the next couple of days.

While we celebrate the Emerald Isle, we’re also watching the forecast. A switch to La Niña for summer 2024 is on the horizon, with forecasts favoring its arrival between June and August.

This news might bring challenges, especially for our growers in hurricane-impact zones in the Southeast. But like Saint Patrick, our industry stands strong against whatever weather comes our way!

More immediately, the annual spring migration from Yuma, AZ, to Salinas, CA, is starting. Just as Saint Patrick brought Christianity to Ireland, strawberries, lettuce, leaf, and cauliflower are pilgrimages from Yuma to the lush fields of the Salinas Valley in California. Over the next six weeks, the supply of weather-weary commodities such as lettuce and strawberries will increase.

ProduceIQ Index:$1.12/pound, up +3.7 percent over prior week

Week #11, ending March 15th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

Though rising, the ProduceIQ Index ($1.12) didn’t increase sharply enough to remain higher than in 2022. 2024 is now the second highest for week #11 historically. Last week marked the seasonal transition from the low winter price point (when Mexico is in full production) to a standard price increase over the next four weeks. Overall, industry supply declines, and prices rise as transitions begin to move northward again.

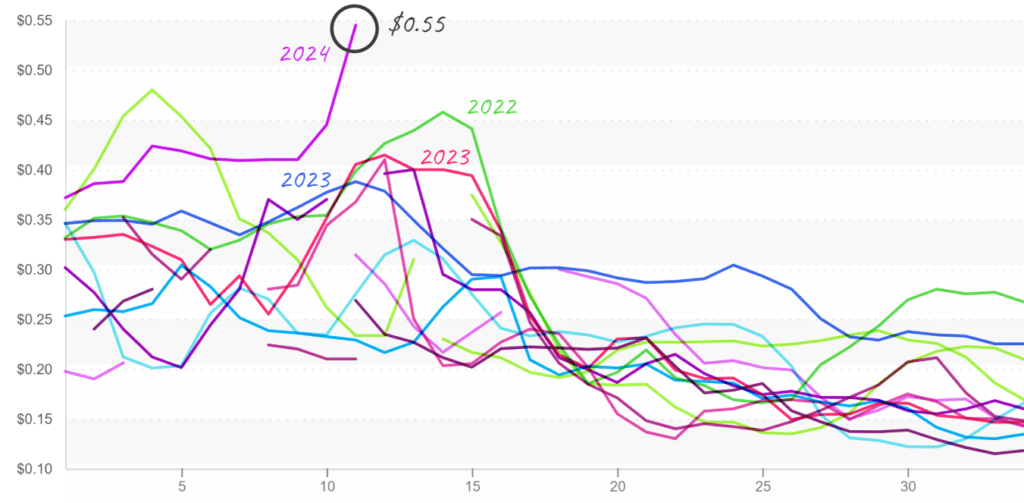

Watermelon prices soar, up +20 percent over the previous week. Short supply on both coasts holds prices at a ten-year high for the fourth consecutive week. Import volume is historically low, and domestic production won’t be able to provide relief for at least three more weeks.

Seedless Watermelon prices in the East rise to $0.55 per pound, reaching new highs, during the gap before Florida is ready.

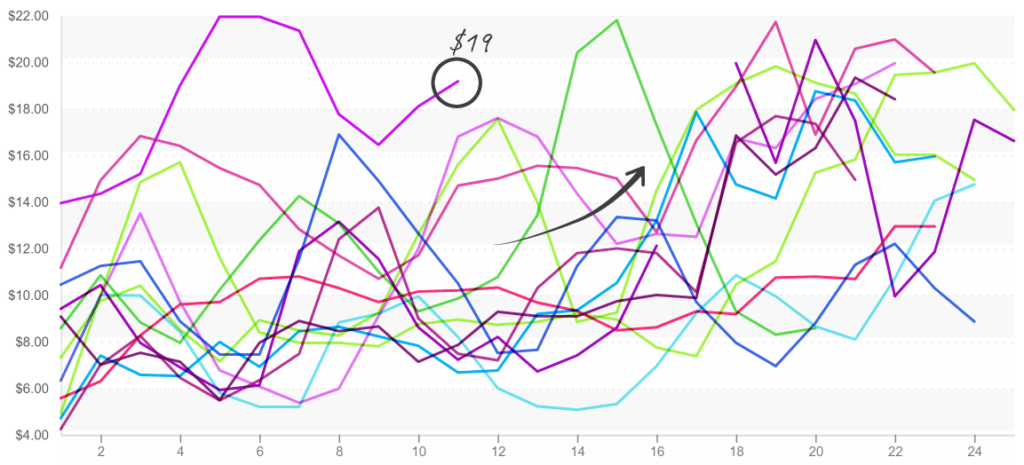

After a few weeks of declining prices, eggplant markets regain upward momentum. Florida’s supply is significantly below the norm for week #10. In Mexico, growers are working to cover the gap. Import supply is tight but should stay steady or even increase through March. Florida’s strong demand and anemic supply will likely keep prices trending above average for the next three weeks.

Eggplant prices in West, $19, are at record highs before prices typically rise.

Lettuce and leaf markets could use some of that Irish luck. Another blast of high wind whipped through growing regions in the Southwest last week, subjecting rain and hail-damaged crops to harsher growing conditions. As a result, the prices of romaine are up +18 percent over the previous week, and the prices of iceberg are up +41 percent.

Hope is just around the corner. The annual spring transition from Yuma to Salinas is underway, and markets will likely feel relief from growers in the Salinas Valley as soon as the end of March.

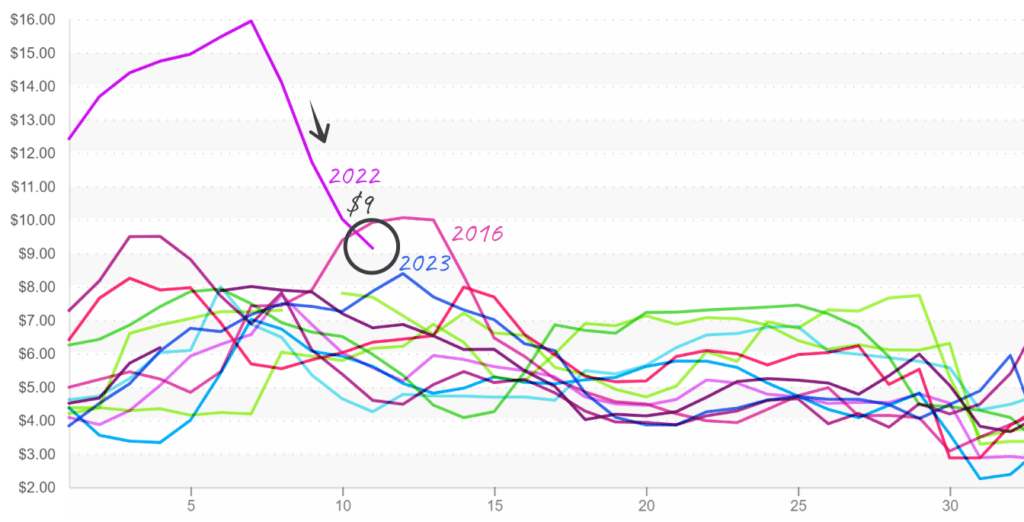

Mango supply is back! South American producers weathered a historically poor production season due to the extreme effects of El Niño. Although markets are still well above average, prices declined for the fourth consecutive week thanks to increasing supply from Mexico, Costa Rica, and Guatemala.

Mango prices from the East (including Texas crossings) are $9 after crashing for four weeks.

ProduceIQ is an online toolset designed to improve the produce trading process for buyers and suppliers. We save you time, expand your opportunities, and provide valuable information to increase your profits.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Happy Saint Patrick’s Day!

As the luck of the Irish would have it, we’re kicking off this week’s produce industry newsletter with updates that might make you feel like you’ve found a pot of gold.

Snow in Colorado might have halted transportation in the Four Corners region, but fear not… Shippers should iron out regional supply chains over the next couple of days.

While we celebrate the Emerald Isle, we’re also watching the forecast. A switch to La Niña for summer 2024 is on the horizon, with forecasts favoring its arrival between June and August.

This news might bring challenges, especially for our growers in hurricane-impact zones in the Southeast. But like Saint Patrick, our industry stands strong against whatever weather comes our way!

More immediately, the annual spring migration from Yuma, AZ, to Salinas, CA, is starting. Just as Saint Patrick brought Christianity to Ireland, strawberries, lettuce, leaf, and cauliflower are pilgrimages from Yuma to the lush fields of the Salinas Valley in California. Over the next six weeks, the supply of weather-weary commodities such as lettuce and strawberries will increase.

ProduceIQ Index:$1.12/pound, up +3.7 percent over prior week

Week #11, ending March 15th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

Though rising, the ProduceIQ Index ($1.12) didn’t increase sharply enough to remain higher than in 2022. 2024 is now the second highest for week #11 historically. Last week marked the seasonal transition from the low winter price point (when Mexico is in full production) to a standard price increase over the next four weeks. Overall, industry supply declines, and prices rise as transitions begin to move northward again.

Watermelon prices soar, up +20 percent over the previous week. Short supply on both coasts holds prices at a ten-year high for the fourth consecutive week. Import volume is historically low, and domestic production won’t be able to provide relief for at least three more weeks.

Seedless Watermelon prices in the East rise to $0.55 per pound, reaching new highs, during the gap before Florida is ready.

After a few weeks of declining prices, eggplant markets regain upward momentum. Florida’s supply is significantly below the norm for week #10. In Mexico, growers are working to cover the gap. Import supply is tight but should stay steady or even increase through March. Florida’s strong demand and anemic supply will likely keep prices trending above average for the next three weeks.

Eggplant prices in West, $19, are at record highs before prices typically rise.

Lettuce and leaf markets could use some of that Irish luck. Another blast of high wind whipped through growing regions in the Southwest last week, subjecting rain and hail-damaged crops to harsher growing conditions. As a result, the prices of romaine are up +18 percent over the previous week, and the prices of iceberg are up +41 percent.

Hope is just around the corner. The annual spring transition from Yuma to Salinas is underway, and markets will likely feel relief from growers in the Salinas Valley as soon as the end of March.

Mango supply is back! South American producers weathered a historically poor production season due to the extreme effects of El Niño. Although markets are still well above average, prices declined for the fourth consecutive week thanks to increasing supply from Mexico, Costa Rica, and Guatemala.

Mango prices from the East (including Texas crossings) are $9 after crashing for four weeks.

ProduceIQ is an online toolset designed to improve the produce trading process for buyers and suppliers. We save you time, expand your opportunities, and provide valuable information to increase your profits.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Mark Campbell is an industry veteran with over 20 years of produce experience. After earning his MBA from Columbia Business School, he spent seven years as CFO for J&J Family of Farms. He later served as CFO advisor to several produce growers, shippers, and distributors. In this role, Mark saw the impediments that prevent produce growers and buyers from trading with greater access and efficiency. This led him to cofound ProduceIQ.