This week marks the beginning of the Northern Hemisphere summer season, and the weather isn’t the only thing heating up. Significant increases in commodities such as raspberries, celery, and sweet corn are balancing the scale and steadying the index. Even with the continued hemorrhaging of cherry prices, average produce prices are flat over the prior week.

ProduceIQ Index: $1.12/pound, flat over prior week

Week #24, ending June 19th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

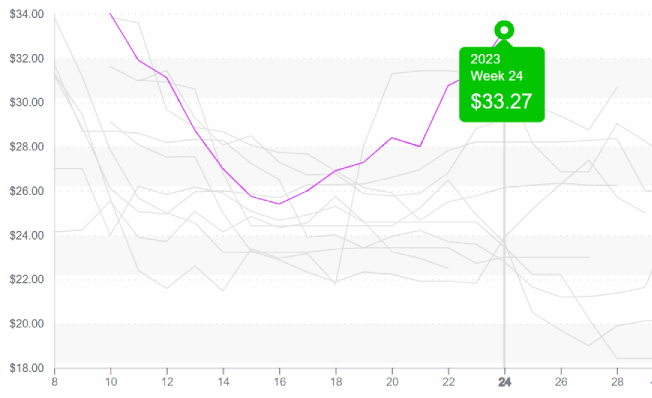

Pear prices are at a ten-year high and are forecasted to rise further due to low supply. Washington is nearly finished, and import supply is snug, especially on smaller-sized fruit. California isn’t expected to provide relief until late July. As a result, expect prices to soar far beyond the historical precedent over the next few weeks.

Pears, 18kg, imported from Chile and Argentina to the East, are at record high prices.

Whoa, avocados. It’s been a hot minute since we’ve had anything to say about you except that you are scandalously cheap. Due to a few factors, Hass prices are up +5 percent over the previous week. Increased demand for the 4th of July celebrations, the delayed start to the new Loca crop, and the seasonal waning of the old crop are all contributing to the disruption of long-stagnant avocado markets.

Don’t fear. You don’t have to ditch your plans to eat guac and chips every Friday night for dinner just yet. Prices are still well below the average, and although they are forecasted to increase a bit more as we approach the 4th of July, the Loca season is only delayed by a week right now.

Hass Avocados, 48ct, crossing Mexico seem cheap at $37; several recent years were “outliers”

Week #24 sweet corn prices are high and likely to increase as new available sources are light before Independence Day. Prices soared another +24 percent over the previous week on high demand and low supply. In the west, California growers are nearly finished with production. In the East, Georgia is working hard to fill the gap, but late planting and reduced acreage have disadvantaged growers.

At $50, celery prices pause for reflection and to enjoy the breathtaking view. Celery production In Oxnard, California, is fading fast, and Salinas, California, dressed in its warmest summer clothes, is sauntering up to the starting line. Seeders are still being reported, reducing yields at the field level and adding pressure to prices.

Good news for celery buyers, volume out of Salinas is up significantly over the previous week and will only increase from here. We hope celery enjoyed the view from the mountaintop. Things are about to move downhill swiftly.

Celery prices (18ct) are falling in the West after a predictable spike during harvest transitions.

At $20, week #24 raspberry prices are at their second highest in ten years. Cool weather in California’s growing regions is stunting supply and forcing prices upwards. Warmer weather is in the forecast, and growers forecast supplies should increase steadily over the next two weeks.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

This week marks the beginning of the Northern Hemisphere summer season, and the weather isn’t the only thing heating up. Significant increases in commodities such as raspberries, celery, and sweet corn are balancing the scale and steadying the index. Even with the continued hemorrhaging of cherry prices, average produce prices are flat over the prior week.

ProduceIQ Index: $1.12/pound, flat over prior week

Week #24, ending June 19th

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

Pear prices are at a ten-year high and are forecasted to rise further due to low supply. Washington is nearly finished, and import supply is snug, especially on smaller-sized fruit. California isn’t expected to provide relief until late July. As a result, expect prices to soar far beyond the historical precedent over the next few weeks.

Pears, 18kg, imported from Chile and Argentina to the East, are at record high prices.

Whoa, avocados. It’s been a hot minute since we’ve had anything to say about you except that you are scandalously cheap. Due to a few factors, Hass prices are up +5 percent over the previous week. Increased demand for the 4th of July celebrations, the delayed start to the new Loca crop, and the seasonal waning of the old crop are all contributing to the disruption of long-stagnant avocado markets.

Don’t fear. You don’t have to ditch your plans to eat guac and chips every Friday night for dinner just yet. Prices are still well below the average, and although they are forecasted to increase a bit more as we approach the 4th of July, the Loca season is only delayed by a week right now.

Hass Avocados, 48ct, crossing Mexico seem cheap at $37; several recent years were “outliers”

Week #24 sweet corn prices are high and likely to increase as new available sources are light before Independence Day. Prices soared another +24 percent over the previous week on high demand and low supply. In the west, California growers are nearly finished with production. In the East, Georgia is working hard to fill the gap, but late planting and reduced acreage have disadvantaged growers.

At $50, celery prices pause for reflection and to enjoy the breathtaking view. Celery production In Oxnard, California, is fading fast, and Salinas, California, dressed in its warmest summer clothes, is sauntering up to the starting line. Seeders are still being reported, reducing yields at the field level and adding pressure to prices.

Good news for celery buyers, volume out of Salinas is up significantly over the previous week and will only increase from here. We hope celery enjoyed the view from the mountaintop. Things are about to move downhill swiftly.

Celery prices (18ct) are falling in the West after a predictable spike during harvest transitions.

At $20, week #24 raspberry prices are at their second highest in ten years. Cool weather in California’s growing regions is stunting supply and forcing prices upwards. Warmer weather is in the forecast, and growers forecast supplies should increase steadily over the next two weeks.

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.

Mark Campbell was introduced to the fresh produce industry as a lender for Farm Credit. After earning his MBA from Columbia Business School, he spent seven years as CFO for J&J Family of Farms and later served as CFO advisor to several produce growers, shippers, and distributors. In this role, Mark saw the impediments that prevent produce growers and buyers to trade with greater access and efficiency. This led him to cofound ProduceIQ.