“Early on in the pandemic, we saw shoppers indulging in more comfort foods,” said Jonna Parker, Team Lead Fresh for IRI. “But 64% of shoppers started 2021 with New Year’s resolutions, according to the IRI Consumer Network survey conducted in January 2021. More than one third, 35%, aim to eat healthier, in general; 35% want to get more exercise; and 29% plan to save more money.”

This is good news for the produce department, with its strong health halo and favorable pricing.

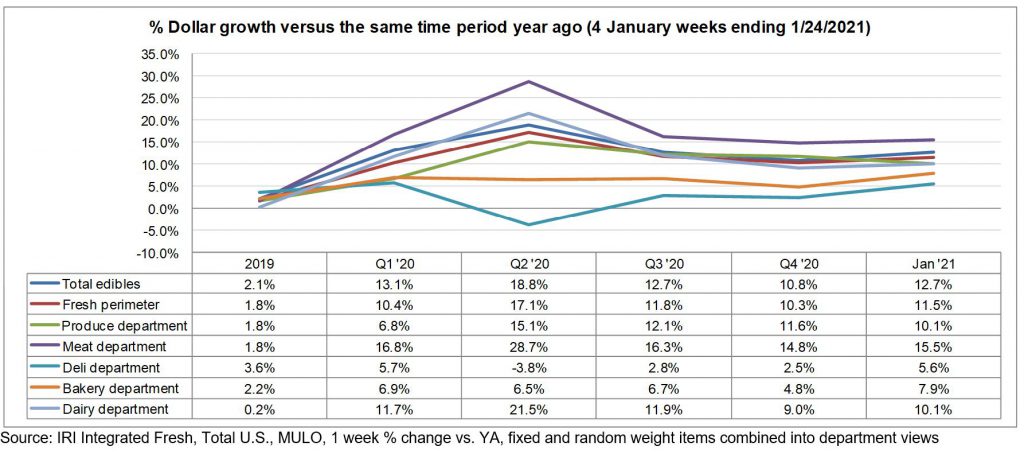

The first four weeks of January saw a recovery of trips to slightly above year ago levels while the basket size remained highly elevated. This resulted in high gains over January 2020 levels for total edibles, which is all food and beverage related items including fresh foods, at +12.7%. This is up significantly from a subdued December retail growth (+8.1%).

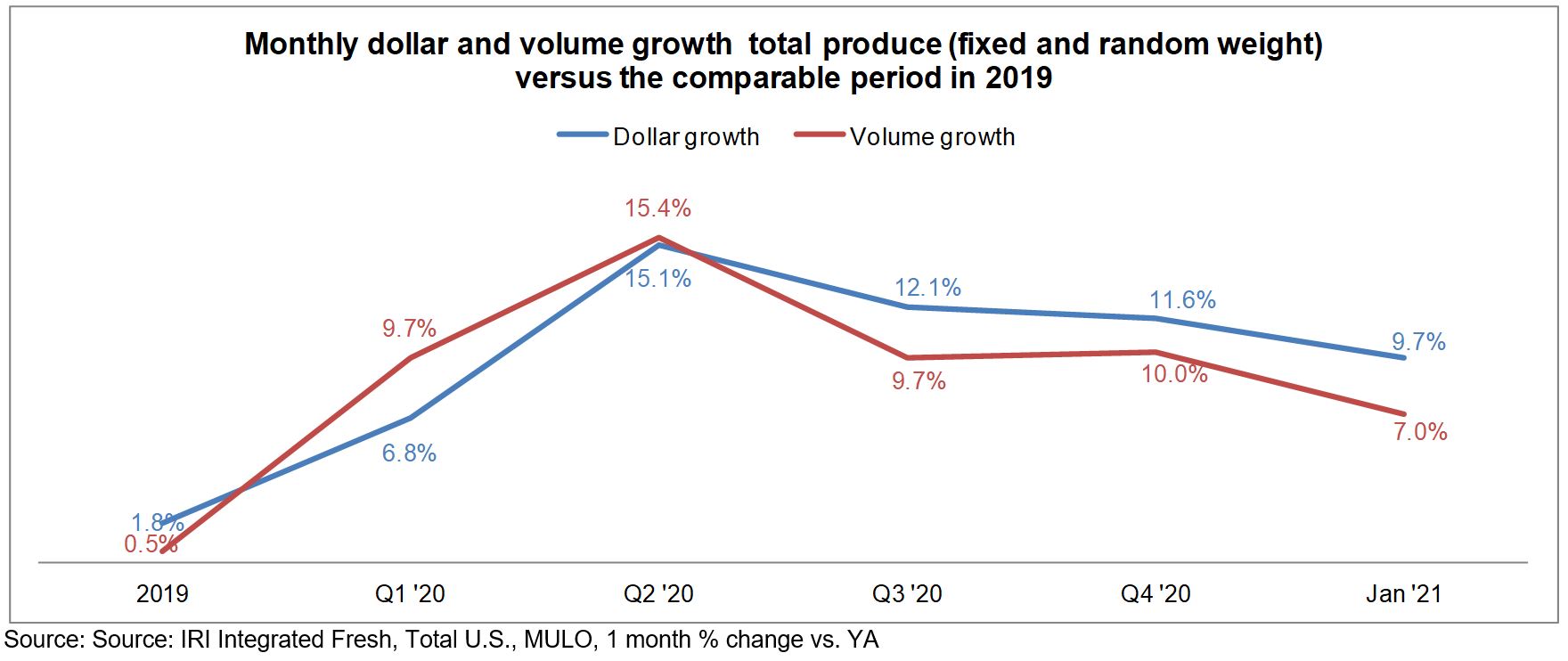

January produce department sales for the five weeks ending 1/31/2021 increased +9.7%, excluding online-only and delivery e-commerce sales that would have been significantly higher than in 2020. IRI shopper research finds that 16% of shoppers are ordering their groceries online more, with 62% opting for click-and-collect fulfillment versus direct-to-home delivery or pure-play online with no physical store. At retail, produce added $576 million versus the comparable period in 2020 for the total fruits and vegetables across the store. As seen throughout the pandemic, frozen fruits and vegetables had the highest growth, but are also the smallest sales of the three temperature zones in retail.

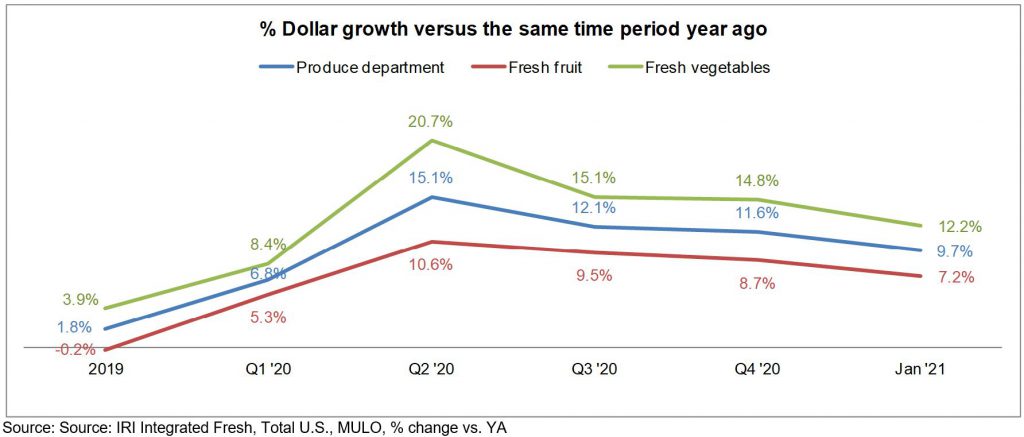

“Produce at retail had a strong January, driven by the two middle weeks ending January 17th and 24th,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “We continue to see highly elevated sales results for vegetables, that are very much in line with the gains seen in the meat department — both pointing at more meals prepared at home. Retail fruit gains have been in the high single digits since the third quarter of 2020 and remain a big opportunity for more at-home snacking, breakfast and lunch.”

“Produce at retail had a strong January, driven by the two middle weeks ending January 17th and 24th,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “We continue to see highly elevated sales results for vegetables, that are very much in line with the gains seen in the meat department — both pointing at more meals prepared at home. Retail fruit gains have been in the high single digits since the third quarter of 2020 and remain a big opportunity for more at-home snacking, breakfast and lunch.”

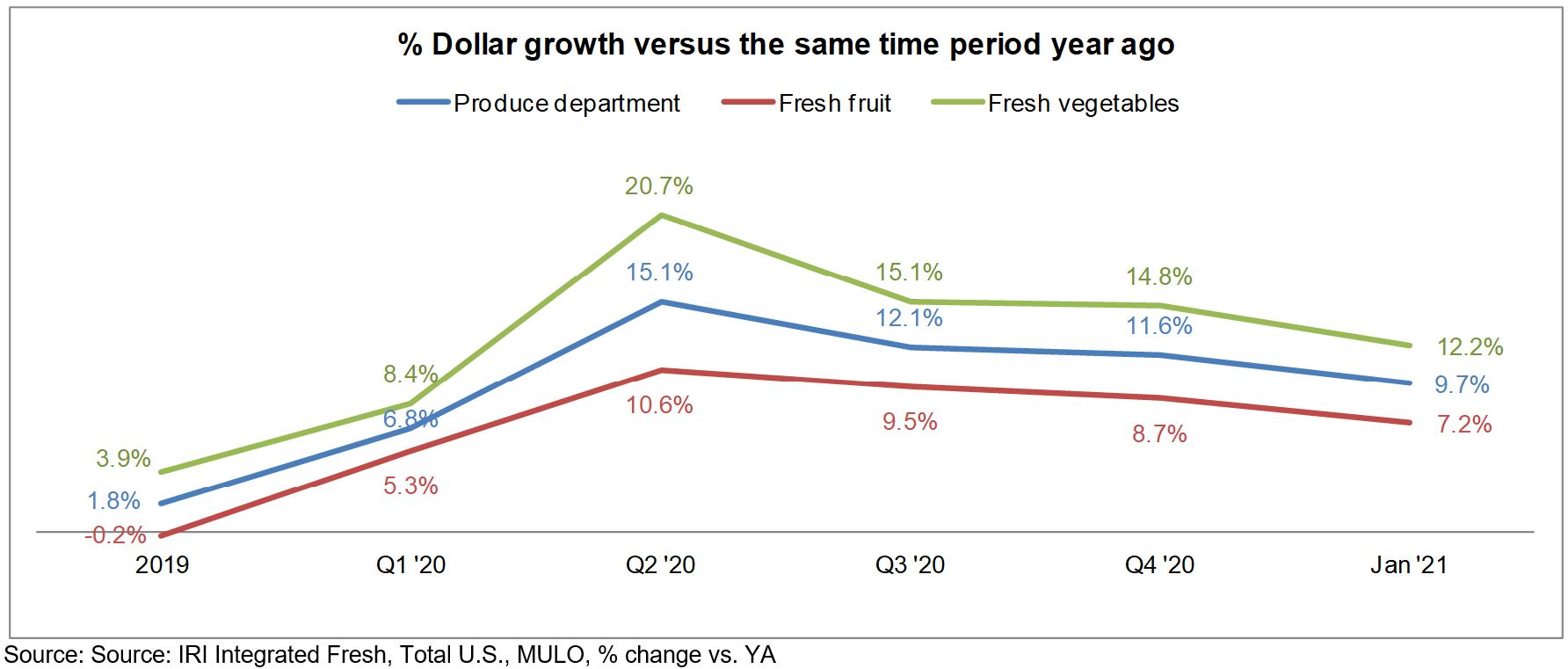

Fresh produce generated $6.3 billion in sales during the January weeks. This reflects $198 million in additional fruit sales and $383 million in additional vegetable sales.

Fresh Share

In 2019, fresh produce sales represented 80.8% of total fruits and vegetables sales across the store. That share fell as low as 76.9% during the first quarter of 2020, pulled down by the March panic buying weeks when many dollars were diverted to frozen and canned. The fresh share briefly recovered in the second and third quarters but as the number of new COVID-19 cases spiked once more in November and December, the fresh share once more dropped to 77.7%. January 2021 showed a slight recovery of the fresh dollar share to 78.1%.

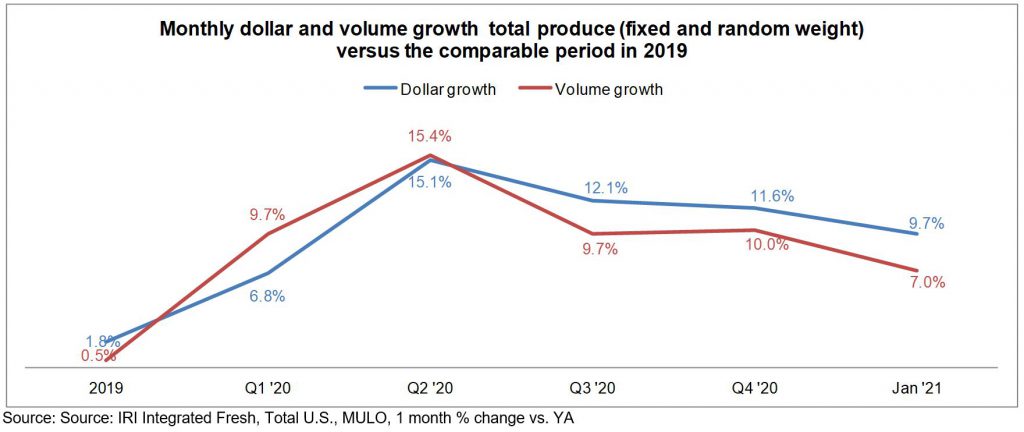

Fresh Produce Dollars versus Volume

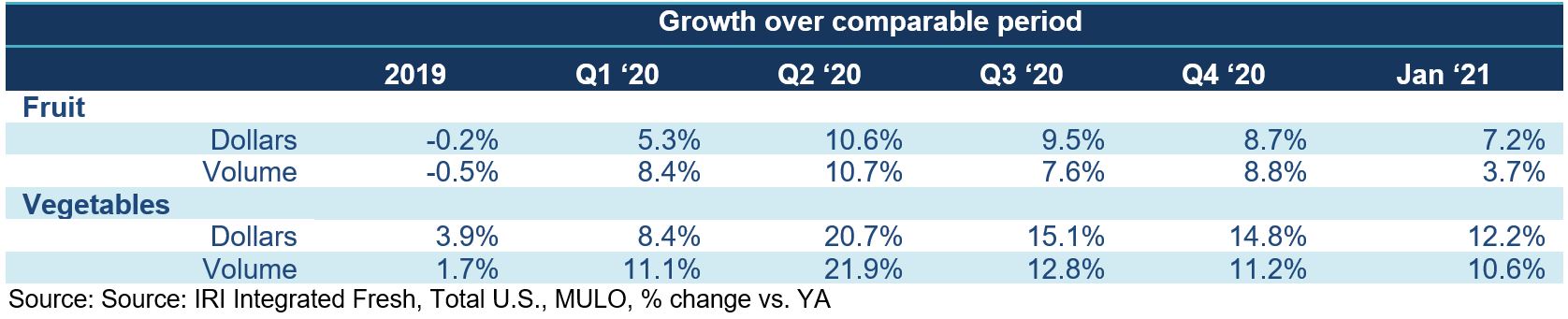

Fresh produce dollars have been outpacing volume since the onset of the pandemic — pointing to inflation as well as premiumization of purchases. In January 2021, the gap between volume and dollar gains widened to 2.7 percentage points, up from 1.6 in the fourth quarter of 2020.

“Retail vegetable growth outpaced fruit in 2019,” said Watson. “Additionally, fruit saw periods of deflation and very low inflation throughout 2020. In January 2021, fruit has the larger volume/dollar gap at 3.5 percentage points versus just 1.6 points for vegetables.”

Absolute Dollar Gains

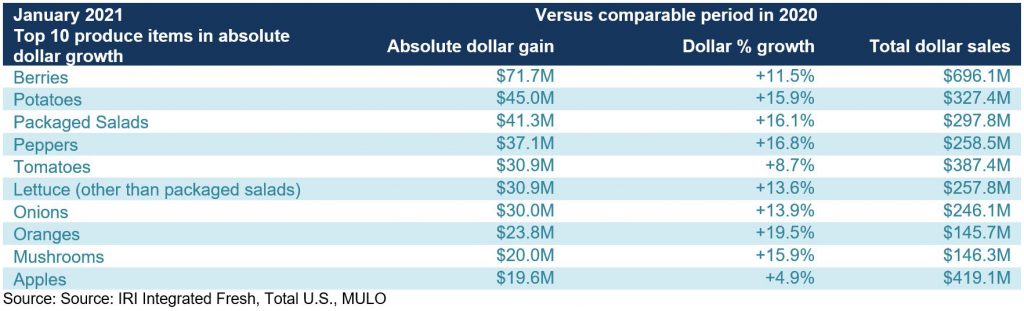

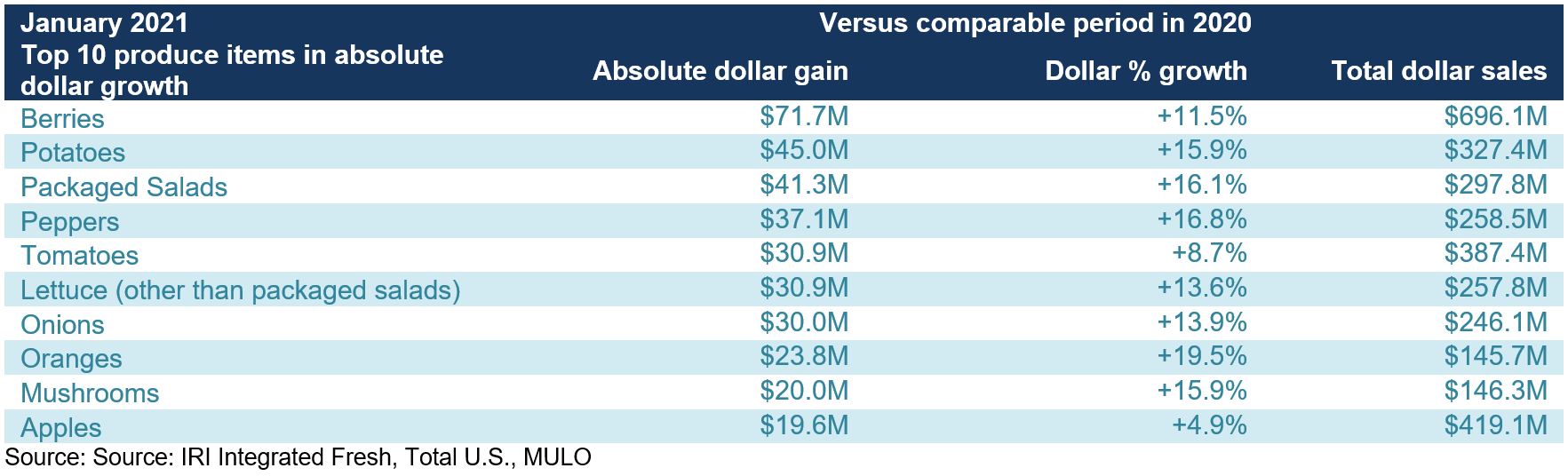

“The January 2021 Top 10 in absolute dollar gains reflects some familiar faces, led by berries, potatoes and salad kits,” said Watson. “To provide some more insight into the enormous popularity of salad kits, we broke out loose lettuce from pre-packaged salads. The latter came in as the number three in terms of the highest absolute dollar gains in January, at +$41.3 million. Oranges climbed to the number seven spot and mushrooms held strong in the ninth spot.”

Fresh Fruit

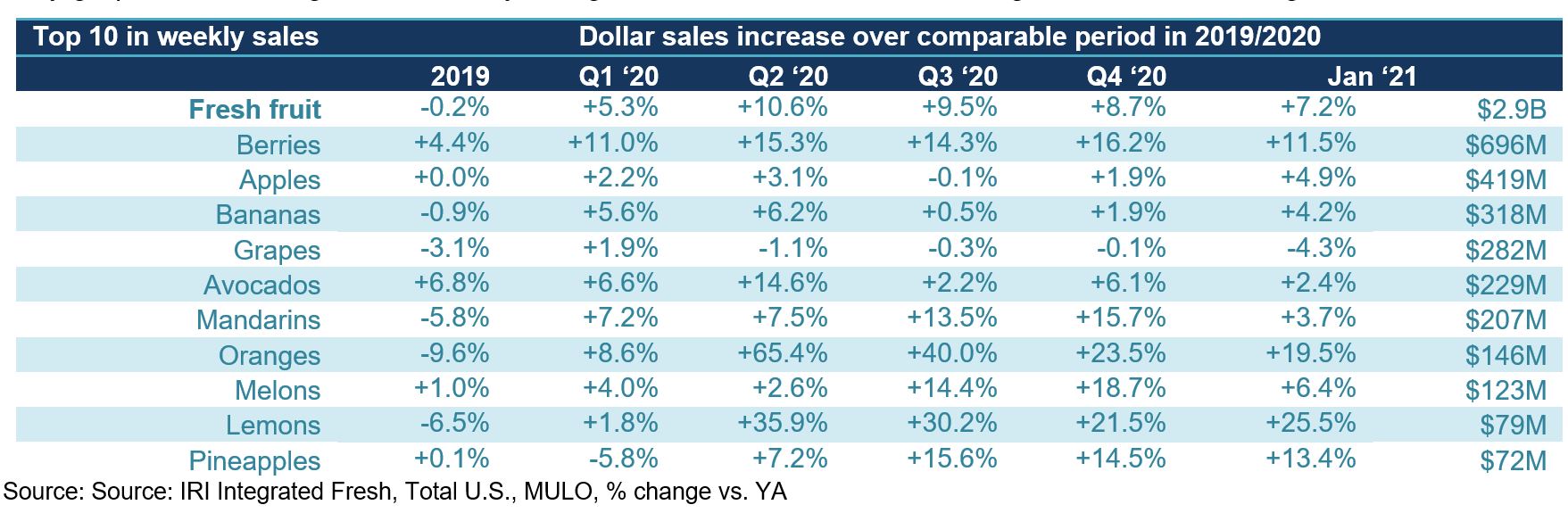

“In fruit, berries remained dominant in sales but the strength of citrus is tremendous,” said Parker. “Citrus fruit was up 13.1% year-over-year, showing consumers’ consistent turn towards foods they perceive to help live healthier lifestyles. Consumers relate citrus to Vitamin-C and, in turn, with boosting their immune systems. Other fruits and vegetables could benefit from leveraging their strengths as many consumers do not off-hand know their power.”

Only grapes lost some ground versus year ago levels while lemons and oranges were the fastest growers.

Fresh Vegetables

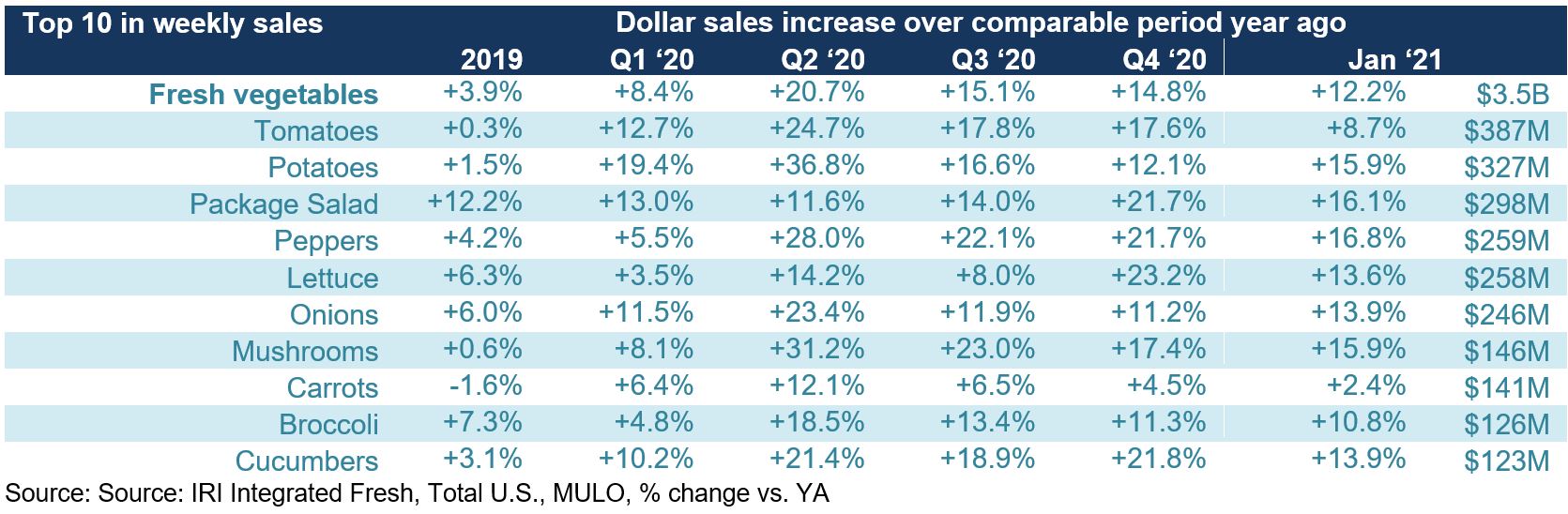

The vegetable side reflects double-digit gains for eight out of the 10 items. “The January top 10 is very similar to what we have been seeing all year,” said Watson. “The dominance of tomatoes, potatoes and packaged salad is astounding, with great strength in size and growth for lettuce, onions and peppers as well. Mushrooms have also been a pandemic powerhouse in retail, placing in the top 10 month after month despite being a much smaller seller.”

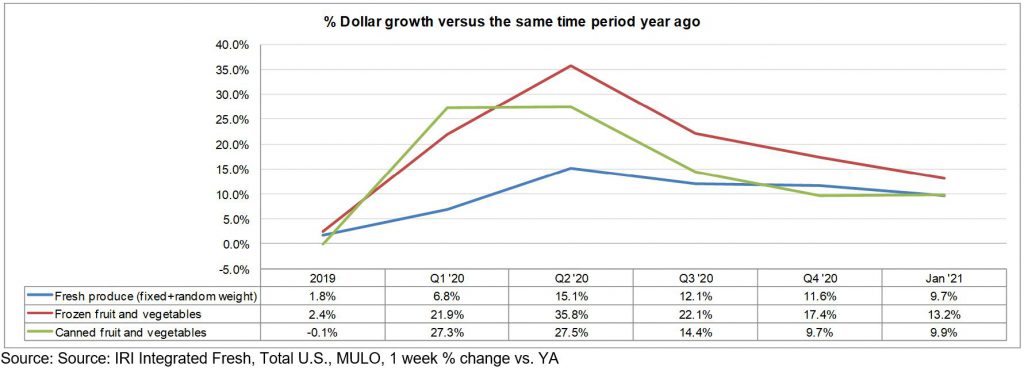

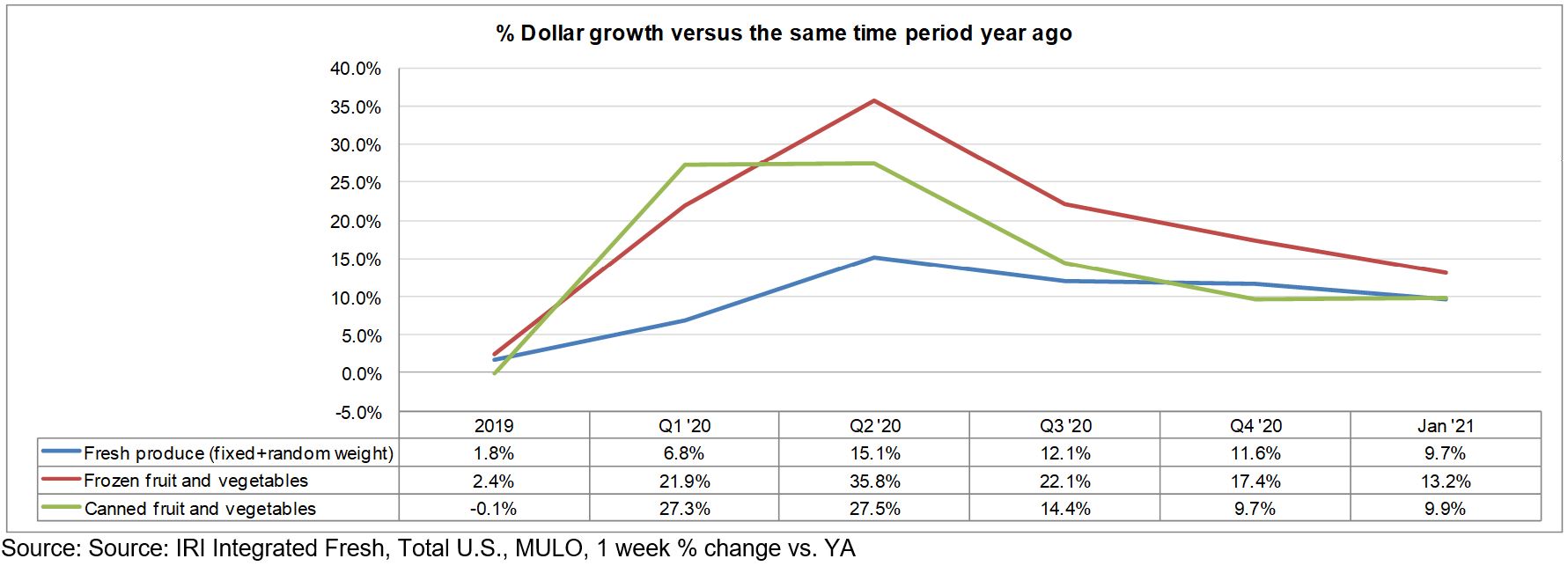

Fresh versus Frozen and Shelf-Stable Fruits and Vegetables

Frozen fruit and vegetables continued their winning streak in the first month of 2021, with an increase of 13.2% over year ago levels. This was, however, the lowest increase since the onset of coronavirus in March 2020. Canned fruit and vegetables remained at fourth quarter sales levels, about 10% above the comparable period a year ago.

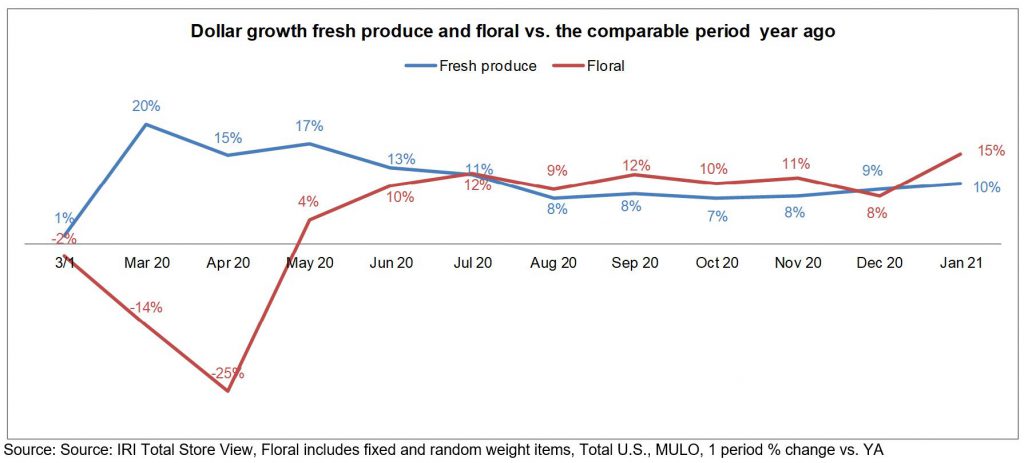

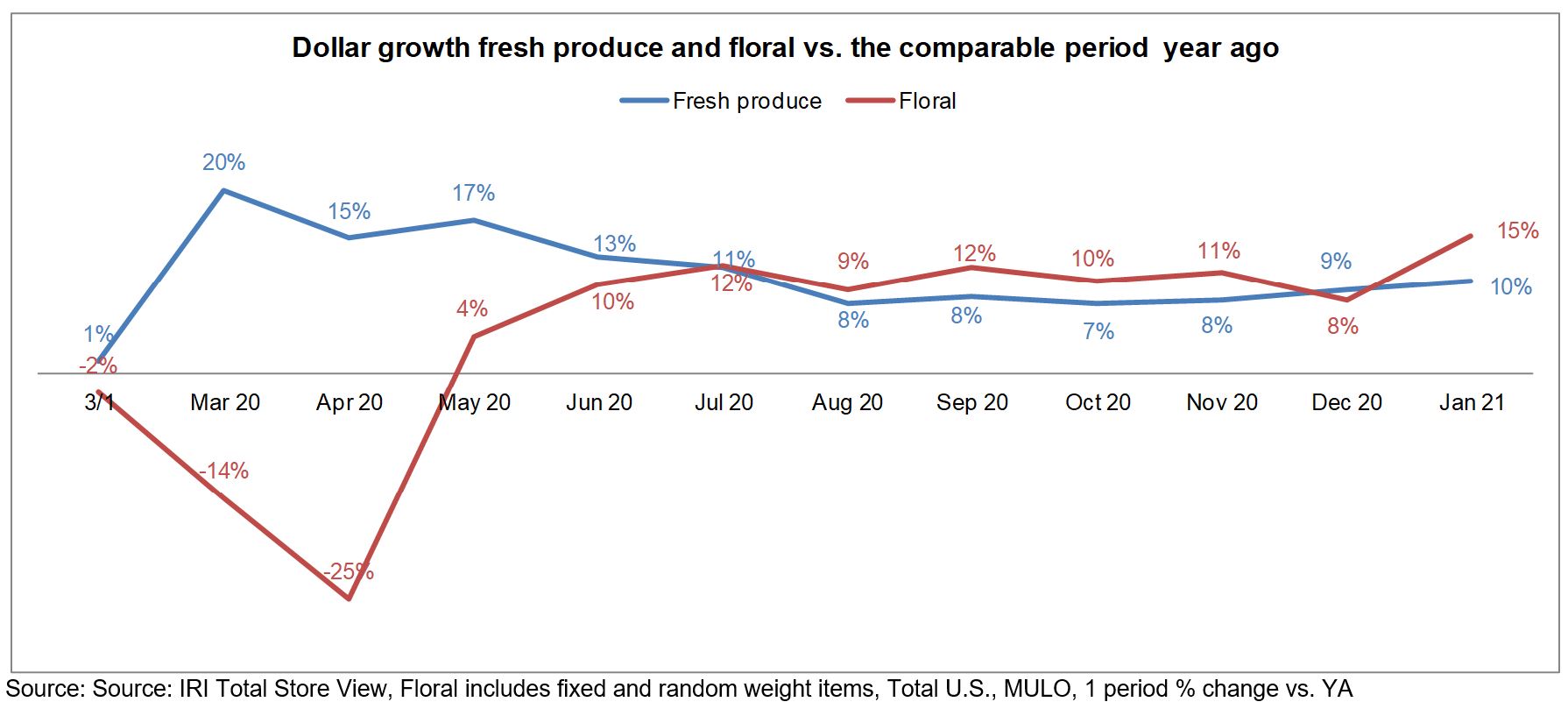

Floral

Floral

Floral sales continued to trend above year ago levels, with a gain of 15% in January 2021 versus the same period year ago. Note: Seasonal and first-time-used codes may not yet be fully counted in Floral as of January. December and prior sales include all available items.

Perimeter Performance

A look across departments for the four weeks ending January 21, 2021 versus year ago shows that total edibles outpaced the perimeter. Fresh department sales were pulled up by a strong month for meat.

What’s Next?

January showed that everyday vegetable demand continued to hold at double-digit above year ago levels, with slightly lower gains for fruit. February has a strong sales opportunity in Valentine’s Day — traditionally a big out-of-home dining occasion, particularly in years where the holiday falls on the weekend. Additionally, continued high counts of COVID-19 cases and cold weather gripping much of the country should spell a more at-home focused occasion than in years past.

Looking further into the future, working from home full time is expected to remain more than twice as high as pre COVID-19: 44% of employed Americans expect to work from home at least once a week after the vaccine is widely distributed and restrictions are lifted, according to the January wave of IRI shopper research.

Likewise, the majority of children were still participating in remote learning in January. About six in 10 school-aged children were in a remote-only model and another 15% in a hybrid approach. Schooling patterns were similar for younger kids, ages 6 to 12 as they were for teens.

Likewise, the majority of children were still participating in remote learning in January. About six in 10 school-aged children were in a remote-only model and another 15% in a hybrid approach. Schooling patterns were similar for younger kids, ages 6 to 12 as they were for teens.

Nearly four in 10 (39%) shoppers expect the health crisis to last more than 12 more months, with an additional 32% expecting it to last another seven to 12 months.

Interest in getting the COVID-19 vaccine grew slightly over the past month:

- 7% have already received the vaccine (one or both doses), up from 3% in December

- 39% plan on getting it as soon as the vaccine is available to them, unchanged from December

- 14% plan to wait a few months or at least six months before taking the vaccine, unchanged from December

- 21% do not plan on taking it, down from 23% in December

- 21% are unsure, unchanged from December.

The next report, covering February, will be released in mid-March. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.

Date ranges:

2019: 52 weeks ending 12/28/2019

Q1 2020: 13 weeks ending 3/29/2020

Q2 2020: 13 weeks ending 6/28/2020

Q3 2020: 13 weeks ending 9/27/2020

Q4 2020: 13 weeks ending 12/27/2020

January: 4 weeks ending 1/31/2021 unless otherwise noted

“Early on in the pandemic, we saw shoppers indulging in more comfort foods,” said Jonna Parker, Team Lead Fresh for IRI. “But 64% of shoppers started 2021 with New Year’s resolutions, according to the IRI Consumer Network survey conducted in January 2021. More than one third, 35%, aim to eat healthier, in general; 35% want to get more exercise; and 29% plan to save more money.”

This is good news for the produce department, with its strong health halo and favorable pricing.

The first four weeks of January saw a recovery of trips to slightly above year ago levels while the basket size remained highly elevated. This resulted in high gains over January 2020 levels for total edibles, which is all food and beverage related items including fresh foods, at +12.7%. This is up significantly from a subdued December retail growth (+8.1%).

January produce department sales for the five weeks ending 1/31/2021 increased +9.7%, excluding online-only and delivery e-commerce sales that would have been significantly higher than in 2020. IRI shopper research finds that 16% of shoppers are ordering their groceries online more, with 62% opting for click-and-collect fulfillment versus direct-to-home delivery or pure-play online with no physical store. At retail, produce added $576 million versus the comparable period in 2020 for the total fruits and vegetables across the store. As seen throughout the pandemic, frozen fruits and vegetables had the highest growth, but are also the smallest sales of the three temperature zones in retail.

“Produce at retail had a strong January, driven by the two middle weeks ending January 17th and 24th,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “We continue to see highly elevated sales results for vegetables, that are very much in line with the gains seen in the meat department — both pointing at more meals prepared at home. Retail fruit gains have been in the high single digits since the third quarter of 2020 and remain a big opportunity for more at-home snacking, breakfast and lunch.”

Fresh produce generated $6.3 billion in sales during the January weeks. This reflects $198 million in additional fruit sales and $383 million in additional vegetable sales.

Fresh Share

In 2019, fresh produce sales represented 80.8% of total fruits and vegetables sales across the store. That share fell as low as 76.9% during the first quarter of 2020, pulled down by the March panic buying weeks when many dollars were diverted to frozen and canned. The fresh share briefly recovered in the second and third quarters but as the number of new COVID-19 cases spiked once more in November and December, the fresh share once more dropped to 77.7%. January 2021 showed a slight recovery of the fresh dollar share to 78.1%.

Fresh Produce Dollars versus Volume

Fresh produce dollars have been outpacing volume since the onset of the pandemic — pointing to inflation as well as premiumization of purchases. In January 2021, the gap between volume and dollar gains widened to 2.7 percentage points, up from 1.6 in the fourth quarter of 2020.

“Retail vegetable growth outpaced fruit in 2019,” said Watson. “Additionally, fruit saw periods of deflation and very low inflation throughout 2020. In January 2021, fruit has the larger volume/dollar gap at 3.5 percentage points versus just 1.6 points for vegetables.”

Absolute Dollar Gains

“The January 2021 Top 10 in absolute dollar gains reflects some familiar faces, led by berries, potatoes and salad kits,” said Watson. “To provide some more insight into the enormous popularity of salad kits, we broke out loose lettuce from pre-packaged salads. The latter came in as the number three in terms of the highest absolute dollar gains in January, at +$41.3 million. Oranges climbed to the number seven spot and mushrooms held strong in the ninth spot.”

Fresh Fruit

“In fruit, berries remained dominant in sales but the strength of citrus is tremendous,” said Parker. “Citrus fruit was up 13.1% year-over-year, showing consumers’ consistent turn towards foods they perceive to help live healthier lifestyles. Consumers relate citrus to Vitamin-C and, in turn, with boosting their immune systems. Other fruits and vegetables could benefit from leveraging their strengths as many consumers do not off-hand know their power.”

Only grapes lost some ground versus year ago levels while lemons and oranges were the fastest growers.

Fresh Vegetables

The vegetable side reflects double-digit gains for eight out of the 10 items. “The January top 10 is very similar to what we have been seeing all year,” said Watson. “The dominance of tomatoes, potatoes and packaged salad is astounding, with great strength in size and growth for lettuce, onions and peppers as well. Mushrooms have also been a pandemic powerhouse in retail, placing in the top 10 month after month despite being a much smaller seller.”

Fresh versus Frozen and Shelf-Stable Fruits and Vegetables

Frozen fruit and vegetables continued their winning streak in the first month of 2021, with an increase of 13.2% over year ago levels. This was, however, the lowest increase since the onset of coronavirus in March 2020. Canned fruit and vegetables remained at fourth quarter sales levels, about 10% above the comparable period a year ago.

Floral

Floral sales continued to trend above year ago levels, with a gain of 15% in January 2021 versus the same period year ago. Note: Seasonal and first-time-used codes may not yet be fully counted in Floral as of January. December and prior sales include all available items.

Perimeter Performance

A look across departments for the four weeks ending January 21, 2021 versus year ago shows that total edibles outpaced the perimeter. Fresh department sales were pulled up by a strong month for meat.

What’s Next?

January showed that everyday vegetable demand continued to hold at double-digit above year ago levels, with slightly lower gains for fruit. February has a strong sales opportunity in Valentine’s Day — traditionally a big out-of-home dining occasion, particularly in years where the holiday falls on the weekend. Additionally, continued high counts of COVID-19 cases and cold weather gripping much of the country should spell a more at-home focused occasion than in years past.

Looking further into the future, working from home full time is expected to remain more than twice as high as pre COVID-19: 44% of employed Americans expect to work from home at least once a week after the vaccine is widely distributed and restrictions are lifted, according to the January wave of IRI shopper research.

Likewise, the majority of children were still participating in remote learning in January. About six in 10 school-aged children were in a remote-only model and another 15% in a hybrid approach. Schooling patterns were similar for younger kids, ages 6 to 12 as they were for teens.

Nearly four in 10 (39%) shoppers expect the health crisis to last more than 12 more months, with an additional 32% expecting it to last another seven to 12 months.

Interest in getting the COVID-19 vaccine grew slightly over the past month:

- 7% have already received the vaccine (one or both doses), up from 3% in December

- 39% plan on getting it as soon as the vaccine is available to them, unchanged from December

- 14% plan to wait a few months or at least six months before taking the vaccine, unchanged from December

- 21% do not plan on taking it, down from 23% in December

- 21% are unsure, unchanged from December.

The next report, covering February, will be released in mid-March. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns. Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes.

Date ranges:

2019: 52 weeks ending 12/28/2019

Q1 2020: 13 weeks ending 3/29/2020

Q2 2020: 13 weeks ending 6/28/2020

Q3 2020: 13 weeks ending 9/27/2020

Q4 2020: 13 weeks ending 12/27/2020

January: 4 weeks ending 1/31/2021 unless otherwise noted

Anne-Marie Roerink is the President of 210 Analytics.

“Produce at retail had a strong January, driven by the two middle weeks ending January 17th and 24th,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “We continue to see highly elevated sales results for vegetables, that are very much in line with the gains seen in the meat department — both pointing at more meals prepared at home. Retail fruit gains have been in the high single digits since the third quarter of 2020 and remain a big opportunity for more at-home snacking, breakfast and lunch.”

“Produce at retail had a strong January, driven by the two middle weeks ending January 17th and 24th,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “We continue to see highly elevated sales results for vegetables, that are very much in line with the gains seen in the meat department — both pointing at more meals prepared at home. Retail fruit gains have been in the high single digits since the third quarter of 2020 and remain a big opportunity for more at-home snacking, breakfast and lunch.”

Likewise, the majority of children were still participating in remote learning in January. About six in 10 school-aged children were in a remote-only model and another 15% in a hybrid approach. Schooling patterns were similar for younger kids, ages 6 to 12 as they were for teens.

Likewise, the majority of children were still participating in remote learning in January. About six in 10 school-aged children were in a remote-only model and another 15% in a hybrid approach. Schooling patterns were similar for younger kids, ages 6 to 12 as they were for teens.