Memorial Day signals the traditional start of the summer grilling season, with meat and produce promotions typically dominating the front page of grocery circulars around the country. This year, however, the tight meat supply created a starring role for fresh produce in many of the weekly ads.

Additionally, social distancing measures prompted smaller gatherings and fewer people traveling for Memorial Day, resulting in continued elevated engagement with grocery retailing, and produce along with it. 210 Analytics, IRI and PMA partnered to understand how retail sales for produce are developing throughout the pandemic and as restaurants around the country are starting to re-open dine-in facilities.

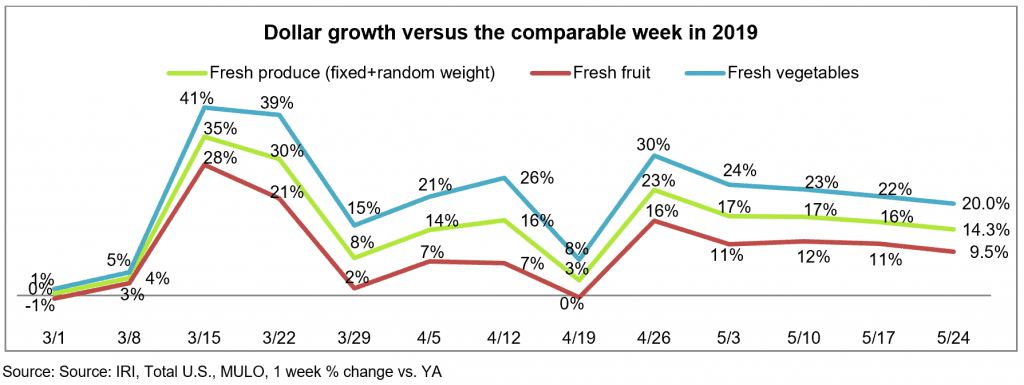

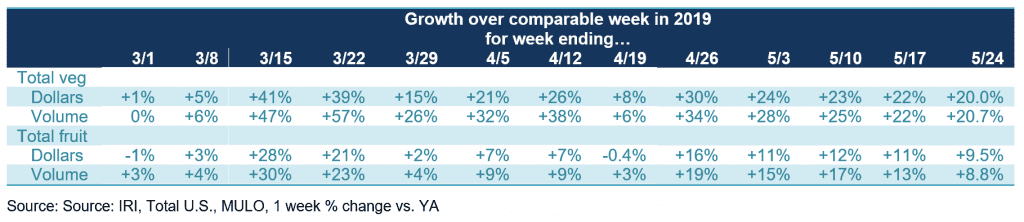

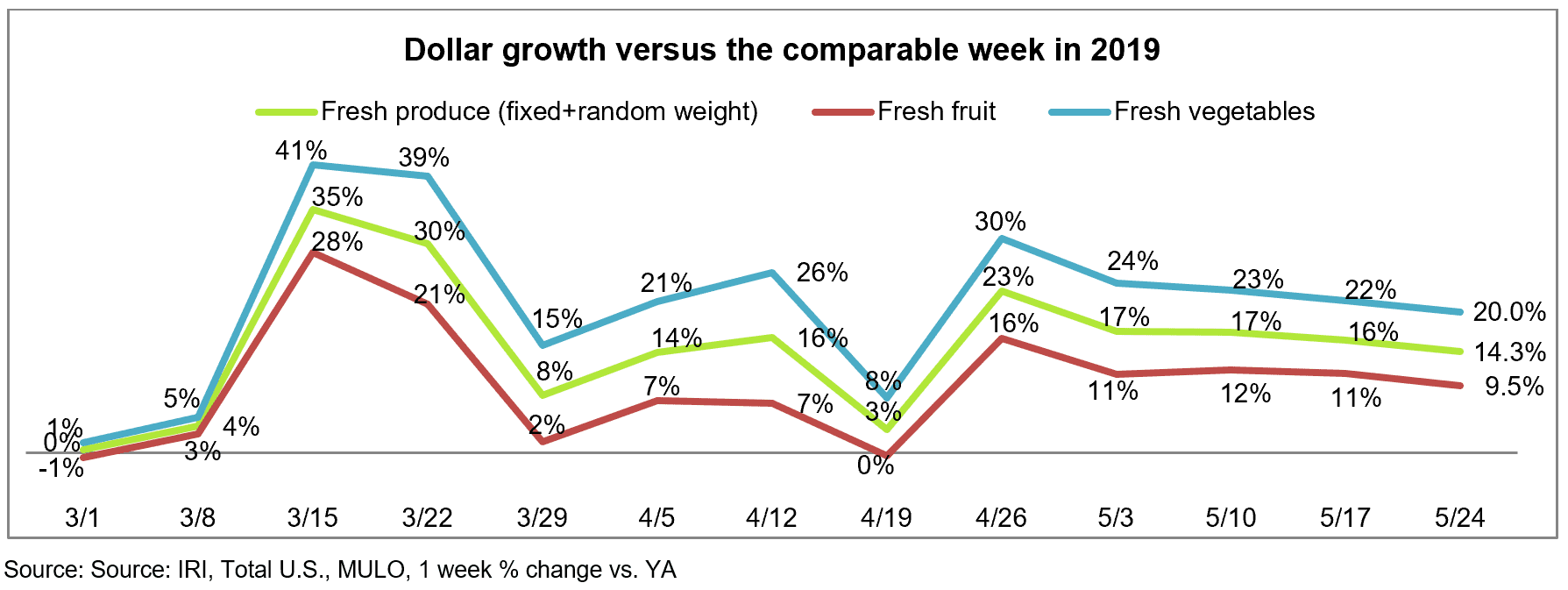

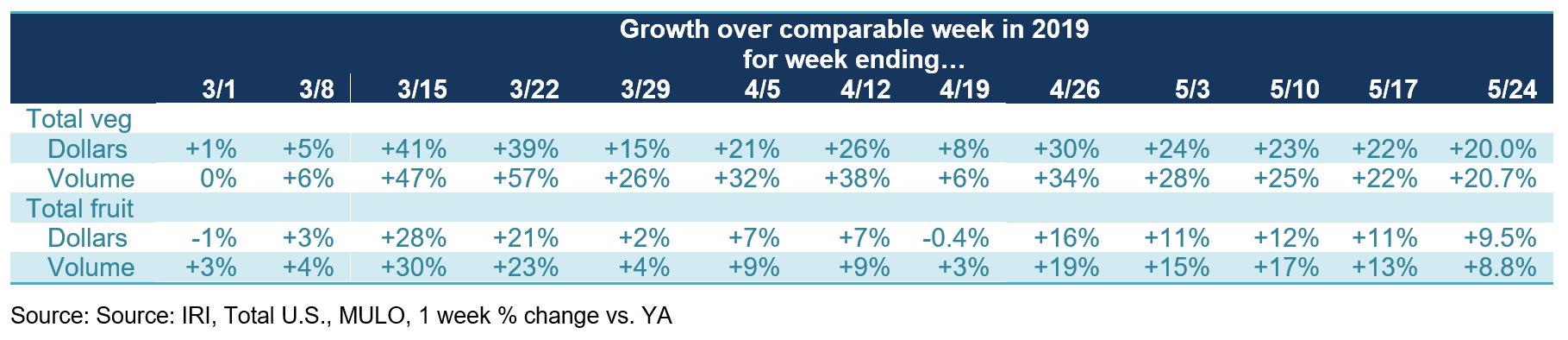

Memorial Day week, elevated everyday and holiday demand drove double-digit produce gains for fresh, frozen and shelf-stable fruits and vegetables. Fresh produce year-over-year growth for the week of May 24 versus the comparable week in 2019 increased 14.3%. Fresh vegetables, up 20.0%, continued to easily outperform fruit (+9.5%). Frozen once more had the highest gains, up 33.8%, despite continued high out-of-stocks and severely limited assortment availability for both frozen vegetables and fruit.

- Fresh produce increased 14.3% over the comparable week in 2019.

- Frozen, +33.8%

- Shelf-stable, +24.6%

Source: IRI, Total US, MULO, % growth vs. year ago week ending May 24, 2020

“Memorial Day week was an important gauge for me to see if summer fruits and vegetables got off to a strong start,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “While we are seeing a bit of erosion in the growth numbers each week, total fresh produce continued to hold in the mid teens, a very welcome pattern for retailers across the country. At the same time, there are many indicators that restaurant demand is strengthening, including a rising number of dinner reservations on OpenTable and continued strong takeout statistics from DoorDash, Uber Eats, Grubhub and others.”

Fresh Produce

Compared with the same week in 2019, fresh produce generated an additional $187 million in sales during the week of May 24, or an additional 122 million pounds. While strong, growth rates have dropped by one to two percentage points each week from the end of April. Fresh vegetables, at +20.0%, boasts double-digit increases for 10 out of the last 11 weeks.

click to enlarge “Our consumer survey work shows that many more consumers cook from scratch and that is a big opportunity for fresh produce,” said Jonna Parker, Team Lead, Fresh for IRI. “Importantly, in our surveys, nearly one-quarter of consumers (23%) predict that they will continue to cook from scratch more than they did pre-pandemic in the upcoming month.

“Our consumer survey work shows that many more consumers cook from scratch and that is a big opportunity for fresh produce,” said Jonna Parker, Team Lead, Fresh for IRI. “Importantly, in our surveys, nearly one-quarter of consumers (23%) predict that they will continue to cook from scratch more than they did pre-pandemic in the upcoming month.

This means shoppers will be looking for tips, inspiration and recipes and the closer we can be to the intersection of inspiration and purchase decisions as brands and retailers, the better our chances for longer term relationships.”

Fresh versus frozen and shelf-stable

Percentage-wise, gains in fresh produce are bound to be lower than frozen and shelf-stable due to its share of total store fruits and vegetables.

“I’m very pleased to see that the fresh share of total fruit and vegetable dollars across the store is almost back to pre-pandemic rates,” said Watson. “In mid-March, consumers were in their stock-up mindset and diverted their dollars from fresh to frozen and canned. The share of fresh to total fruit and vegetable sales across the store stood as low as 70%, but in the latest week fresh is back to 82%.”

click to enlarge Concern over the safety of fresh produce lingers for some shoppers. Some commented on the Retail Feedback Group’s Constant Customer Feedback (CCF) program this week.

Concern over the safety of fresh produce lingers for some shoppers. Some commented on the Retail Feedback Group’s Constant Customer Feedback (CCF) program this week.

One shopper wrote, “I will not be back to this store until everyone is required to wear a mask. People could have sneezed all over the produce products like the apples and broccoli that are not covered in plastic. This lack of concern for the safety of others is totally uncalled for. Merely put a sign out front at the only entrance that says if you do not have a mask, you cannot enter our store.”

Another disagreed with worries over fresh produce and said, “I get that some people want to see produce in bags, but I prefer to pick my own, especially avocados, tomatoes and squash. I just wash it well at home like I always do and do not believe we need all that extra packaging.”

Other shoppers commented on being pleased with the quality, assortment and freshness of the produce assortment at their stores.

“This trip the produce was much more plentiful than it had been. The quality looked good and pleased to see that fresh herbs were back and organic was in stock.”

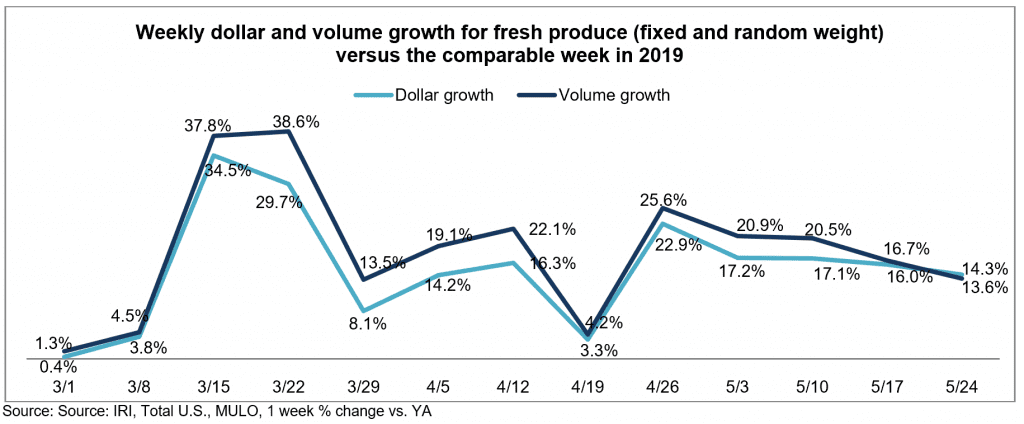

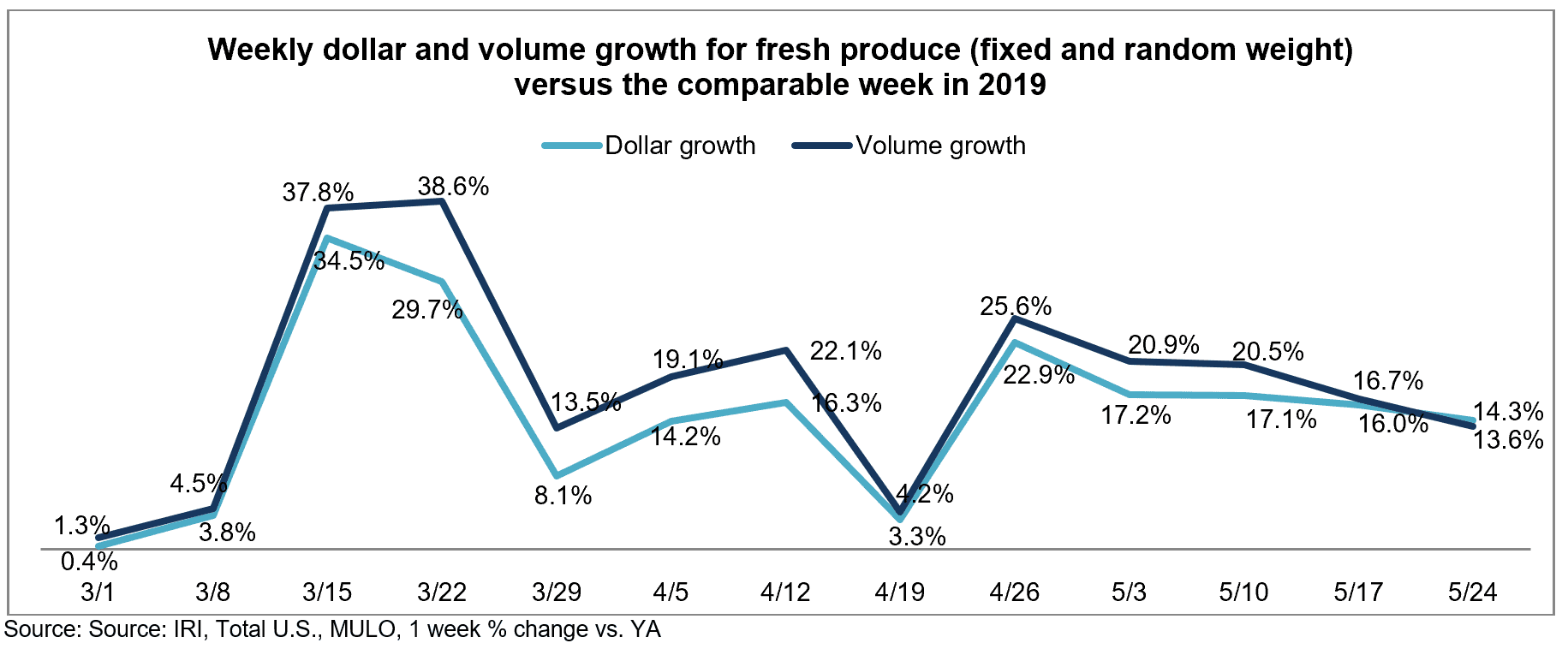

Dollars versus Volume

After narrowing significantly the week of May 17, the volume/dollar gap that once stood at nearly 9 percentage points completely vanished the week of May 24. In fact, dollars tracked slightly ahead of pounds for the first time.

“Where other departments have seen inflation throughout the pandemic, prices were flat or down for most fresh fruits and vegetables until this week,” Parker said.

click to enlarge Vegetables still saw volume growth tracking ahead of dollars the week of May 24 versus the comparable week in 2019. However, the volume/dollar gap for fresh vegetables has come down to just 0.7 percentage points. In fruit, dollar gains outpaced volume gains for the first time since the onset of coronavirus in the U.S., albeit by less than 1 point.

Vegetables still saw volume growth tracking ahead of dollars the week of May 24 versus the comparable week in 2019. However, the volume/dollar gap for fresh vegetables has come down to just 0.7 percentage points. In fruit, dollar gains outpaced volume gains for the first time since the onset of coronavirus in the U.S., albeit by less than 1 point.

click to enlarge

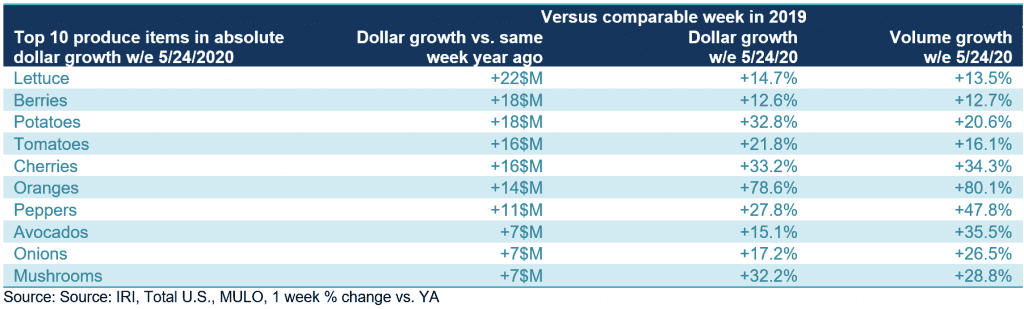

The top three growth items in terms of absolute dollar gains over the same week in 2019 were lettuce, berries and potatoes. While the volume/dollar gap has dissolved overall, there are several vegetables were significant gaps remain, including peppers, avocados and onions.

click to enlarge “On the fruit side, we see strong demand across the board expressed in high volume gains versus last year. However, in some areas, ample supply is still suppressing prices which means there are continued significant volume/dollar gaps for items such as avocados (22 point gap), grapes (14 points) and apples (8 points),” said Watson. “For others, supply and demand are starting to balance out more and for items such as tangerines, mangoes, papaya and peaches dollar gains are actually outpacing volume.”

“On the fruit side, we see strong demand across the board expressed in high volume gains versus last year. However, in some areas, ample supply is still suppressing prices which means there are continued significant volume/dollar gaps for items such as avocados (22 point gap), grapes (14 points) and apples (8 points),” said Watson. “For others, supply and demand are starting to balance out more and for items such as tangerines, mangoes, papaya and peaches dollar gains are actually outpacing volume.”

On the vegetable side, peppers, onions, Brussels sprouts and cauliflower are all vegetables with significantly higher volume than dollar gains. However, potatoes, corn and asparagus are examples of vegetables were dollar gains outpaced volume growth.

“The strong demand and dollar delivery of sweet corn is an important sign that summer sales are off to a strong start,” said Watson.

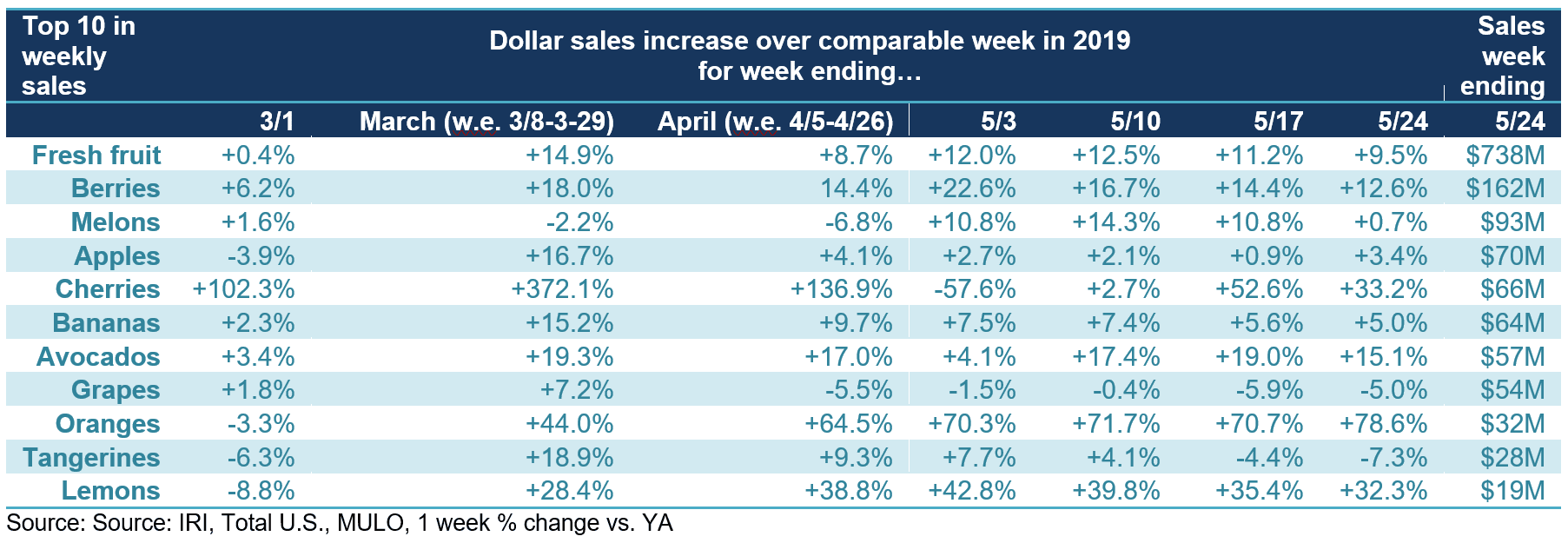

Fresh Fruit

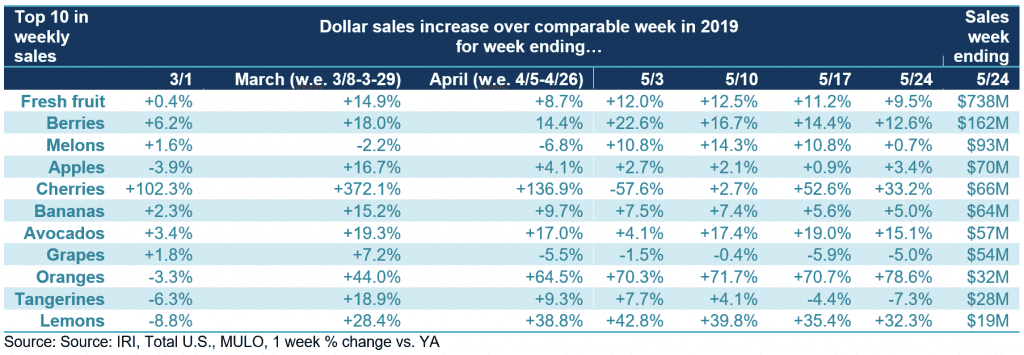

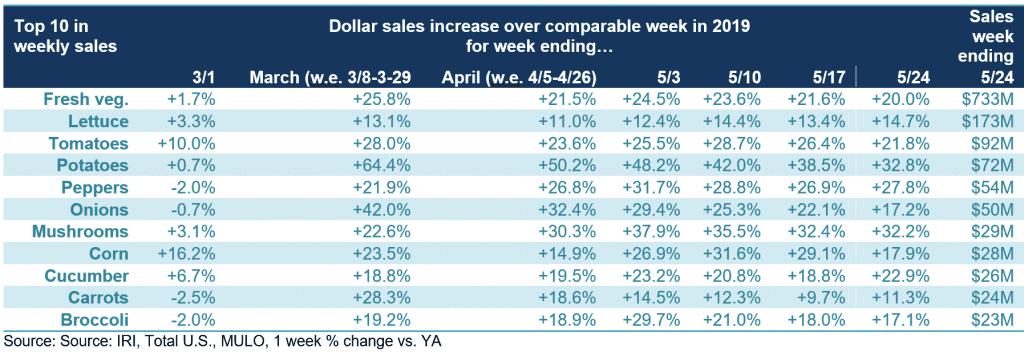

“Fruit gains lost about one point and dropped just below +10% the week of May 24 versus the same week year ago,” said Parker. “Oranges continue to be on fire with another week of nearly 80% growth and cherries built on a strong start of the season and became the fourth highest seller among fresh fruits at nearly $66 million.” Five out of the top 10 items in terms of dollar sales saw double-digit increases during the week of May 24 versus the comparable week in 2019, whereas grape and tangerine sales continued to see dollar sales pressure.

click to enlarge

Fresh vegetables

All top 10 vegetable items in terms of dollar sales gained double-digits the week ending May 24. “From day one we have seen vegetables take big leaps over last year’s sales and that remained true for Memorial Day weekend also,” said Parker. “We even saw accelerated gains for several top 10 vegetables, including lettuce, cucumbers and carrots.”

Lettuce was the top sales category and was the top contributor in absolute dollar growth in vegetables, adding $22 million in sales versus the comparable week in 2019.

click to enlarge

Sales gains for fresh cut salad also accelerated over the week ending May 24, to 13% over year ago. That was the largest gain for the month of May.

click to enlarge

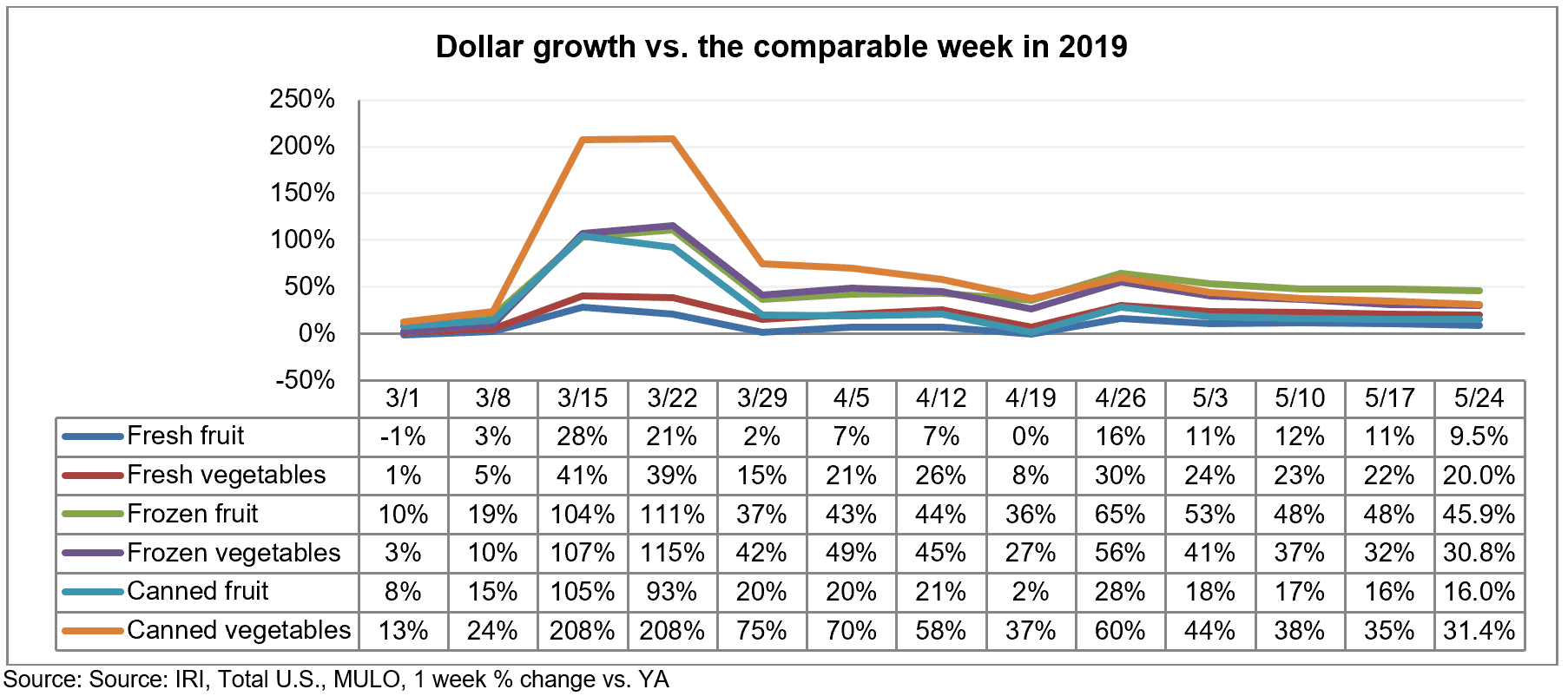

Fresh Versus Frozen and Shelf-Stable Fruits and Vegetables

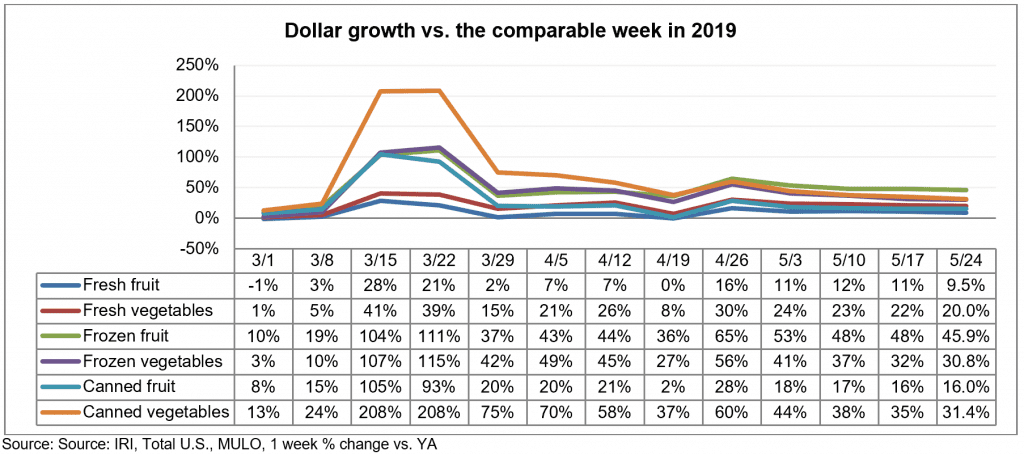

While gains in frozen continued to outpace those in fresh and canned, frozen is also the smallest of the three areas and the difference has grown significantly smaller since the two panic buying weeks. Both frozen and canned fruit and vegetables had double-digit growth once more, with frozen fruit reporting the highest gains, at +45.9%.

click to enlarge

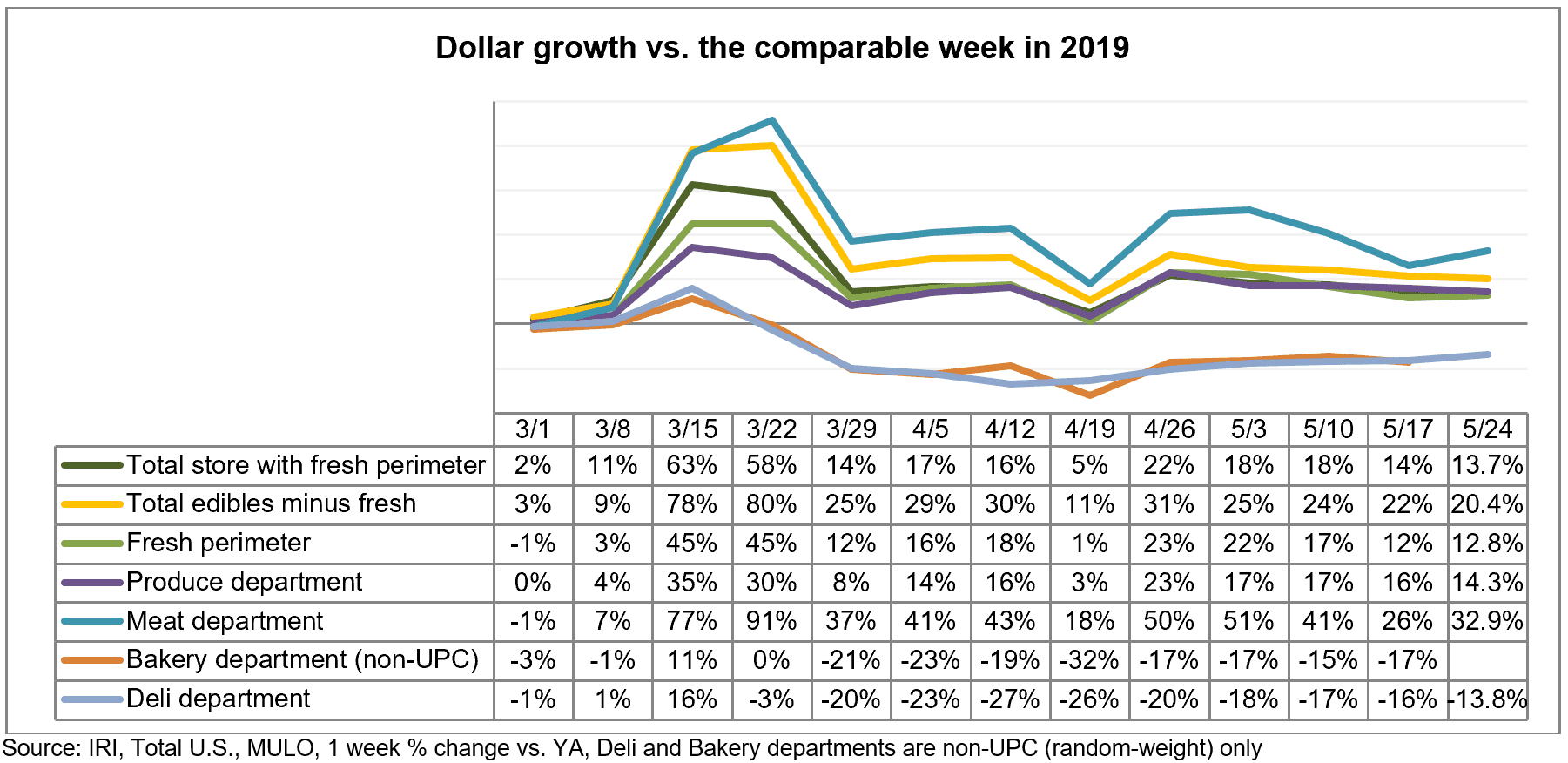

Perimeter performance

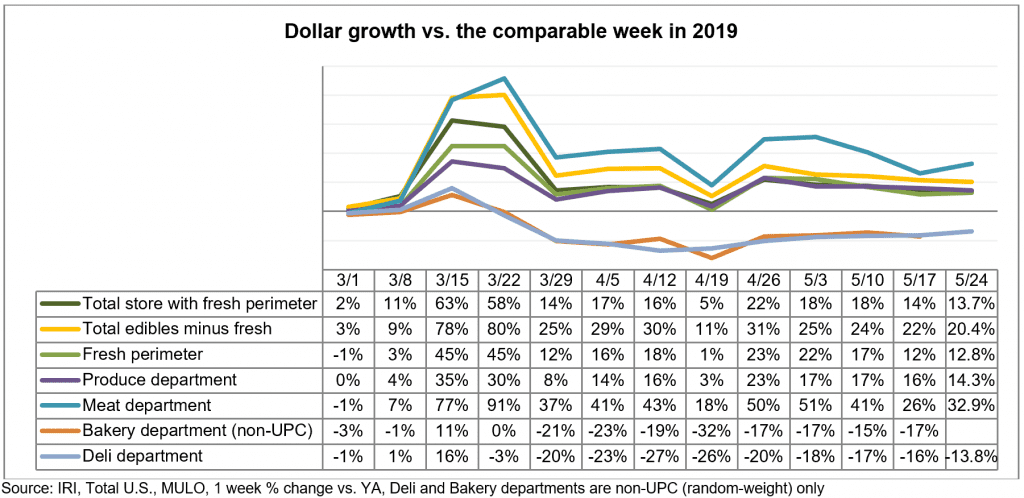

Gains for center-store edibles continued to outpace those in fresh during the week of May 24. Meat and produce sales were highly elevated, but these gains were pulled down by deli prepared and the in-store (fresh) bakery that have struggled since the end of March as quarantines ramped up.

Click to enlarge.

What’s next?

The next sales report, covering week 12 of coronavirus’ affected shopping patterns, is the final week of May. For some states, that coincided with the start of summer vacation. Since mid-March, the closing of schools and colleges brought many more meal occasions to at-home. Now, those altered COVID-19 consumption patterns will go up against summer vacation consumption patterns of prior years. Meanwhile, the relaxation of the stay-at-home executive orders looks different from state to state.

Many have relaxed mandates allowing some consumers to shop, dine and work out of home. The economic recovery along with the foodservice engagement in those states will be very telling for the likely level of demand at food retailing for the foreseeable future. Given the limited seating, economic pressure and perhaps some latent social anxiety, it is likely that grocery and fresh produce demand will continue to sit well above the 2019 baseline. The IRI consumer survey wave of May 15 to 17, found that 23% plan or have gone back to eating out at restaurants like they were pre-pandemic once they are/were able, but 24% plan to wait a few weeks after the restrictions are lifted and 50% believe they will wait a month or more before dining out.

Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes. 210 Analytics and IRI will continue to provide weekly updates as sales trends develop, made possible by PMA. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns.

Memorial Day signals the traditional start of the summer grilling season, with meat and produce promotions typically dominating the front page of grocery circulars around the country. This year, however, the tight meat supply created a starring role for fresh produce in many of the weekly ads.

Additionally, social distancing measures prompted smaller gatherings and fewer people traveling for Memorial Day, resulting in continued elevated engagement with grocery retailing, and produce along with it. 210 Analytics, IRI and PMA partnered to understand how retail sales for produce are developing throughout the pandemic and as restaurants around the country are starting to re-open dine-in facilities.

Memorial Day week, elevated everyday and holiday demand drove double-digit produce gains for fresh, frozen and shelf-stable fruits and vegetables. Fresh produce year-over-year growth for the week of May 24 versus the comparable week in 2019 increased 14.3%. Fresh vegetables, up 20.0%, continued to easily outperform fruit (+9.5%). Frozen once more had the highest gains, up 33.8%, despite continued high out-of-stocks and severely limited assortment availability for both frozen vegetables and fruit.

- Fresh produce increased 14.3% over the comparable week in 2019.

- Frozen, +33.8%

- Shelf-stable, +24.6%

Source: IRI, Total US, MULO, % growth vs. year ago week ending May 24, 2020

“Memorial Day week was an important gauge for me to see if summer fruits and vegetables got off to a strong start,” said Joe Watson, VP of Membership and Engagement for the Produce Marketing Association (PMA). “While we are seeing a bit of erosion in the growth numbers each week, total fresh produce continued to hold in the mid teens, a very welcome pattern for retailers across the country. At the same time, there are many indicators that restaurant demand is strengthening, including a rising number of dinner reservations on OpenTable and continued strong takeout statistics from DoorDash, Uber Eats, Grubhub and others.”

Fresh Produce

Compared with the same week in 2019, fresh produce generated an additional $187 million in sales during the week of May 24, or an additional 122 million pounds. While strong, growth rates have dropped by one to two percentage points each week from the end of April. Fresh vegetables, at +20.0%, boasts double-digit increases for 10 out of the last 11 weeks.

click to enlarge“Our consumer survey work shows that many more consumers cook from scratch and that is a big opportunity for fresh produce,” said Jonna Parker, Team Lead, Fresh for IRI. “Importantly, in our surveys, nearly one-quarter of consumers (23%) predict that they will continue to cook from scratch more than they did pre-pandemic in the upcoming month.

This means shoppers will be looking for tips, inspiration and recipes and the closer we can be to the intersection of inspiration and purchase decisions as brands and retailers, the better our chances for longer term relationships.”

Fresh versus frozen and shelf-stable

Percentage-wise, gains in fresh produce are bound to be lower than frozen and shelf-stable due to its share of total store fruits and vegetables.

“I’m very pleased to see that the fresh share of total fruit and vegetable dollars across the store is almost back to pre-pandemic rates,” said Watson. “In mid-March, consumers were in their stock-up mindset and diverted their dollars from fresh to frozen and canned. The share of fresh to total fruit and vegetable sales across the store stood as low as 70%, but in the latest week fresh is back to 82%.”

click to enlargeConcern over the safety of fresh produce lingers for some shoppers. Some commented on the Retail Feedback Group’s Constant Customer Feedback (CCF) program this week.

One shopper wrote, “I will not be back to this store until everyone is required to wear a mask. People could have sneezed all over the produce products like the apples and broccoli that are not covered in plastic. This lack of concern for the safety of others is totally uncalled for. Merely put a sign out front at the only entrance that says if you do not have a mask, you cannot enter our store.”

Another disagreed with worries over fresh produce and said, “I get that some people want to see produce in bags, but I prefer to pick my own, especially avocados, tomatoes and squash. I just wash it well at home like I always do and do not believe we need all that extra packaging.”

Other shoppers commented on being pleased with the quality, assortment and freshness of the produce assortment at their stores.

“This trip the produce was much more plentiful than it had been. The quality looked good and pleased to see that fresh herbs were back and organic was in stock.”

Dollars versus Volume

After narrowing significantly the week of May 17, the volume/dollar gap that once stood at nearly 9 percentage points completely vanished the week of May 24. In fact, dollars tracked slightly ahead of pounds for the first time.

“Where other departments have seen inflation throughout the pandemic, prices were flat or down for most fresh fruits and vegetables until this week,” Parker said.

click to enlargeVegetables still saw volume growth tracking ahead of dollars the week of May 24 versus the comparable week in 2019. However, the volume/dollar gap for fresh vegetables has come down to just 0.7 percentage points. In fruit, dollar gains outpaced volume gains for the first time since the onset of coronavirus in the U.S., albeit by less than 1 point.

click to enlarge

The top three growth items in terms of absolute dollar gains over the same week in 2019 were lettuce, berries and potatoes. While the volume/dollar gap has dissolved overall, there are several vegetables were significant gaps remain, including peppers, avocados and onions.

click to enlarge“On the fruit side, we see strong demand across the board expressed in high volume gains versus last year. However, in some areas, ample supply is still suppressing prices which means there are continued significant volume/dollar gaps for items such as avocados (22 point gap), grapes (14 points) and apples (8 points),” said Watson. “For others, supply and demand are starting to balance out more and for items such as tangerines, mangoes, papaya and peaches dollar gains are actually outpacing volume.”

On the vegetable side, peppers, onions, Brussels sprouts and cauliflower are all vegetables with significantly higher volume than dollar gains. However, potatoes, corn and asparagus are examples of vegetables were dollar gains outpaced volume growth.

“The strong demand and dollar delivery of sweet corn is an important sign that summer sales are off to a strong start,” said Watson.

Fresh Fruit

“Fruit gains lost about one point and dropped just below +10% the week of May 24 versus the same week year ago,” said Parker. “Oranges continue to be on fire with another week of nearly 80% growth and cherries built on a strong start of the season and became the fourth highest seller among fresh fruits at nearly $66 million.” Five out of the top 10 items in terms of dollar sales saw double-digit increases during the week of May 24 versus the comparable week in 2019, whereas grape and tangerine sales continued to see dollar sales pressure.

click to enlarge

Fresh vegetables

All top 10 vegetable items in terms of dollar sales gained double-digits the week ending May 24. “From day one we have seen vegetables take big leaps over last year’s sales and that remained true for Memorial Day weekend also,” said Parker. “We even saw accelerated gains for several top 10 vegetables, including lettuce, cucumbers and carrots.”

Lettuce was the top sales category and was the top contributor in absolute dollar growth in vegetables, adding $22 million in sales versus the comparable week in 2019.

click to enlarge

Sales gains for fresh cut salad also accelerated over the week ending May 24, to 13% over year ago. That was the largest gain for the month of May.

click to enlarge

Fresh Versus Frozen and Shelf-Stable Fruits and Vegetables

While gains in frozen continued to outpace those in fresh and canned, frozen is also the smallest of the three areas and the difference has grown significantly smaller since the two panic buying weeks. Both frozen and canned fruit and vegetables had double-digit growth once more, with frozen fruit reporting the highest gains, at +45.9%.

click to enlarge

Perimeter performance

Gains for center-store edibles continued to outpace those in fresh during the week of May 24. Meat and produce sales were highly elevated, but these gains were pulled down by deli prepared and the in-store (fresh) bakery that have struggled since the end of March as quarantines ramped up.

Click to enlarge.

What’s next?

The next sales report, covering week 12 of coronavirus’ affected shopping patterns, is the final week of May. For some states, that coincided with the start of summer vacation. Since mid-March, the closing of schools and colleges brought many more meal occasions to at-home. Now, those altered COVID-19 consumption patterns will go up against summer vacation consumption patterns of prior years. Meanwhile, the relaxation of the stay-at-home executive orders looks different from state to state.

Many have relaxed mandates allowing some consumers to shop, dine and work out of home. The economic recovery along with the foodservice engagement in those states will be very telling for the likely level of demand at food retailing for the foreseeable future. Given the limited seating, economic pressure and perhaps some latent social anxiety, it is likely that grocery and fresh produce demand will continue to sit well above the 2019 baseline. The IRI consumer survey wave of May 15 to 17, found that 23% plan or have gone back to eating out at restaurants like they were pre-pandemic once they are/were able, but 24% plan to wait a few weeks after the restrictions are lifted and 50% believe they will wait a month or more before dining out.

Please recognize the continued dedication of the entire grocery and produce supply chains, from farm to retailer, on keeping the produce supply flowing during these unprecedented times. #produce #joyoffresh #SupermarketSuperHeroes. 210 Analytics and IRI will continue to provide weekly updates as sales trends develop, made possible by PMA. We encourage you to contact Joe Watson, PMA’s Vice President of Membership and Engagement, at jwatson@pma.com with any questions or concerns.

Anne-Marie Roerink is the President of 210 Analytics.

“Our consumer survey work shows that many more consumers cook from scratch and that is a big opportunity for fresh produce,” said Jonna Parker, Team Lead, Fresh for IRI. “Importantly, in our surveys, nearly one-quarter of consumers (23%) predict that they will continue to cook from scratch more than they did pre-pandemic in the upcoming month.

“Our consumer survey work shows that many more consumers cook from scratch and that is a big opportunity for fresh produce,” said Jonna Parker, Team Lead, Fresh for IRI. “Importantly, in our surveys, nearly one-quarter of consumers (23%) predict that they will continue to cook from scratch more than they did pre-pandemic in the upcoming month. Concern over the safety of fresh produce lingers for some shoppers. Some commented on the Retail Feedback Group’s Constant Customer Feedback (CCF) program this week.

Concern over the safety of fresh produce lingers for some shoppers. Some commented on the Retail Feedback Group’s Constant Customer Feedback (CCF) program this week. Vegetables still saw volume growth tracking ahead of dollars the week of May 24 versus the comparable week in 2019. However, the volume/dollar gap for fresh vegetables has come down to just 0.7 percentage points. In fruit, dollar gains outpaced volume gains for the first time since the onset of coronavirus in the U.S., albeit by less than 1 point.

Vegetables still saw volume growth tracking ahead of dollars the week of May 24 versus the comparable week in 2019. However, the volume/dollar gap for fresh vegetables has come down to just 0.7 percentage points. In fruit, dollar gains outpaced volume gains for the first time since the onset of coronavirus in the U.S., albeit by less than 1 point.

“On the fruit side, we see strong demand across the board expressed in high volume gains versus last year. However, in some areas, ample supply is still suppressing prices which means there are continued significant volume/dollar gaps for items such as avocados (22 point gap), grapes (14 points) and apples (8 points),” said Watson. “For others, supply and demand are starting to balance out more and for items such as tangerines, mangoes, papaya and peaches dollar gains are actually outpacing volume.”

“On the fruit side, we see strong demand across the board expressed in high volume gains versus last year. However, in some areas, ample supply is still suppressing prices which means there are continued significant volume/dollar gaps for items such as avocados (22 point gap), grapes (14 points) and apples (8 points),” said Watson. “For others, supply and demand are starting to balance out more and for items such as tangerines, mangoes, papaya and peaches dollar gains are actually outpacing volume.”