The swing of Spring is well underway and much of the fresh produce industry is transitioning to new harvesting regions.

Though prices broadly are flat, volume continues to accelerate as spring crops begin harvest.

Prices are holding due to increased demand as April weather allows northern states to experience the outdoors.

Blue Book has teamed with ProduceIQ BB #:368175 to bring the ProduceIQ Index to its readers. The index provides a produce industry price benchmark using 40 top commodities to provide data for decision making.

ProduceIQ Index: $1.10 /pound, +0.9 percent over prior week

Week #14, ending April 9th

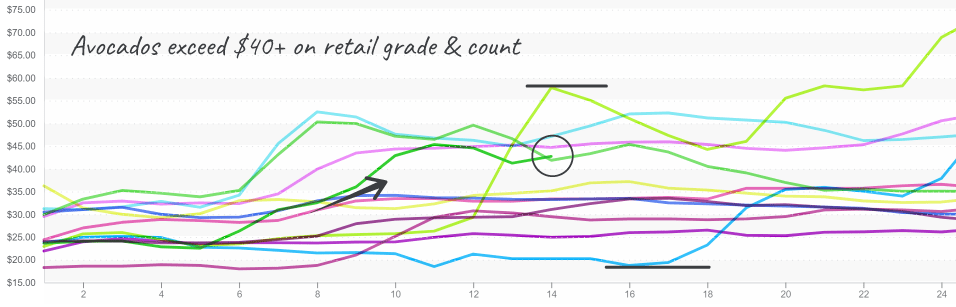

Mexican avocado growers are enjoying another year of continued high prices, much to the chagrin of retail and foodservice buyers. Deciding to reduce harvest levels to accelerate prices into the $40+ range is arguably short-sighted hubris, akin to Icarus flying too close to the sun.

The number of retail stores with ads on avocados has reduced sharply. Long-term, Mexican growers are vulnerable to getting singed by new acreage being planted in Peru and Colombia.

Retail demand lessens at high price points, and retailers will avoid promotions, substitute shelf space, and proactively seek contracts from new growing regions.

Keith Slattery, CEO of Stonehill Produce, BB #:159843 writes in his latest industry update, “The net sum of all that time in the funhouse is massive FATIGUE at all levels of the industry that has many turning the page on Mexico.”

Buyers, weary of the volatility, look favorably towards Peru and California for supply agreements.

Hass avocados maintain high prices as a market with supply-side discipline.

Thanks to Florida’s Spring harvest, sweet corn markets are down -23 percent. Although still at elevated levels, after a winter of tight supplies, sweet corn prices are finally finding their way back towards historical norms.

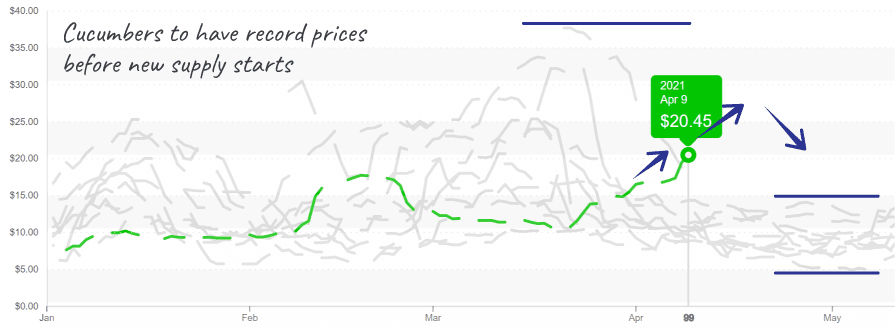

The cucumber gap is not yet filled; prices rise again, up 16 percent. Market prices will remain elevated until production in Florida and Mexico’s Sonora region accelerate. Cucumber prices are being quoted in the high $20 range by those without much fruit to sell.

Tomatoes, down -11 percent, have bottomed once again at the TSA floor prices. Plentiful supply and average demand have tomato sellers holding cucumbers hostage. The ransom price for cucumbers, an accompanying order of tomatoes.

Cucumbers continue price climb, bucking historical norms.

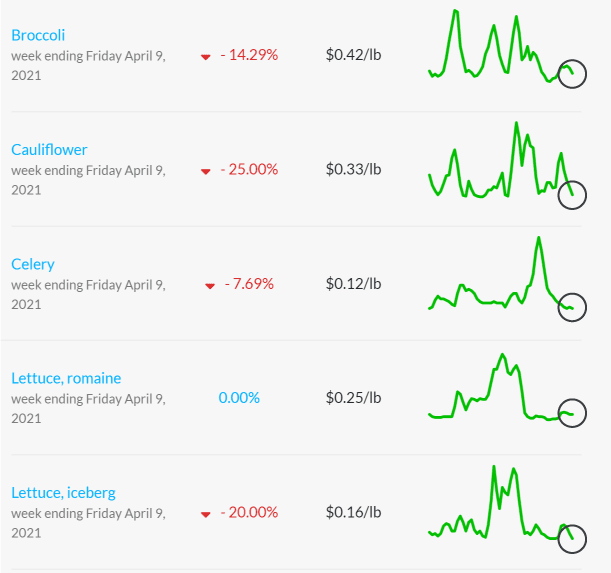

Wet vegetable category, including broccoli, cauliflower and celery, is at the lowest prices for week #14 since 2012. All commodities are experiencing abundant supply, and prices are expected to remain steady in the coming weeks.

Lettuces, iceberg and romaine, are also trending low. Iceberg is down again, -20 percent. Transition from Yuma to Salinas is almost complete. Supply from two overlapping harvest regions has challenged logistics in what is already extremely difficult freight environment. If you can find a truck, excellent quality and plentiful supply makes California produce a buy.

California veg struggles with low prices during the transition northward.

Please visit our online marketplace here and enjoy free access to our market tools.

Hope to connect with you at the CPMA Fresh Week starting today!

ProduceIQ Index

The ProduceIQ Index is the fresh produce industry’s only shipping point price index. It represents the industry-wide price per pound at the location of packing for domestic produce, and at the port of U.S. entry for imported produce.

ProduceIQ uses 40 top commodities to represent the industry. The Index weights each commodity dynamically, by season, as a function of the weekly 5-year rolling average Sales. Sales are calculated using the USDA’s Agricultural Marketing Service for movement and price data. The Index serves as a fair benchmark for industry price performance.